COMMENT: Escalating Middle East conflict raises risks of renewed European energy shock

After US President Donald Trump failed to deliver on his promise of a quick end to the conflict in Iran, the chances of a renewed European energy shock are rising quickly, Ricardo Amaro, Lead Economist at Oxford Economics said in a note emailed to clients.

In a repeat of the 2022 energy shock, spiking prices would weigh on European growth and push inflation higher.

“Although we try to see through the extreme daily fluctuations in oil prices, the Iran conflict implies upside risk for our oil price and inflation forecasts and downside risk for our GDP growth projections,” Amaro said.

Oil markets have become highly volatile amid uncertainty over the conflict’s trajectory. Brent crude has swung from above $110 a barrel to below $90 and back above $100 within days, as traders react to breaking news headlines and unhinged presidential tweets. Expectations over supply disruptions and geopolitical escalation change hourly. “Traders remain hostage to the news flow,” Amaro said, noting that volatility has spread across commodities, bonds and equities.

Heavily dependent on energy imports, Europe is one of the most exposed of all major markets to price volatility. Oxford Economics’ baseline assumes oil prices will ease towards $80 a barrel, but alternative scenarios point to more persistent shocks.

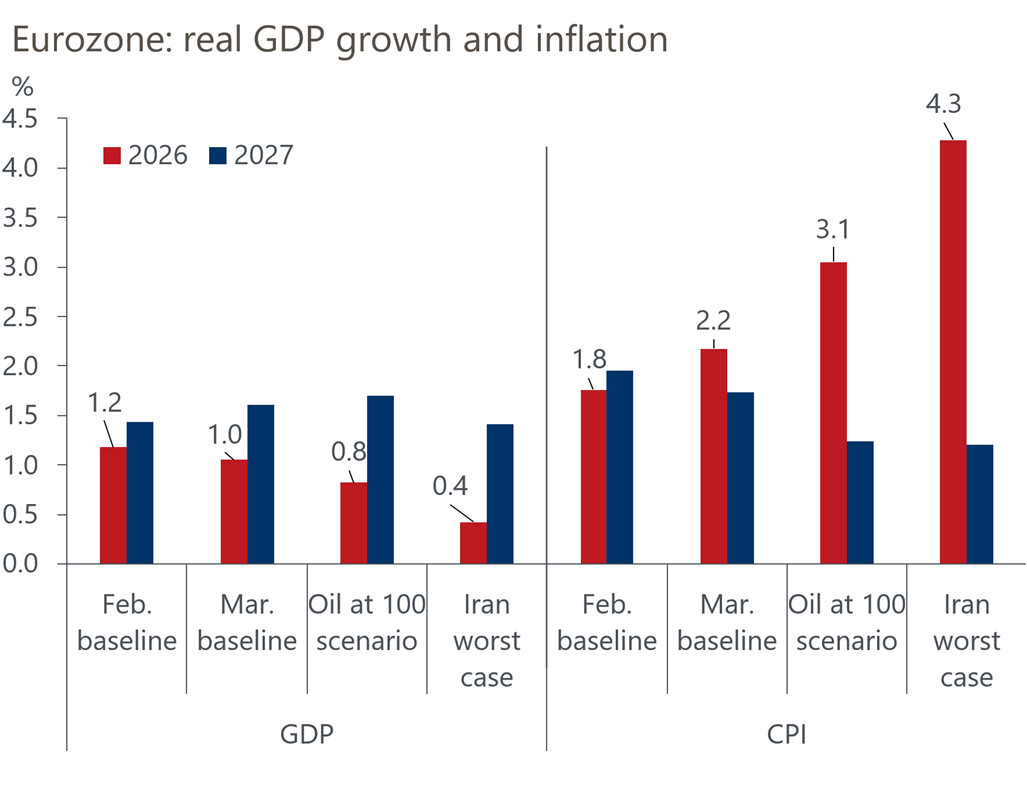

“If prices remain around $100 per barrel for a couple of months, along with other secondary effects, we estimate Eurozone GDP would be 0.3% lower by the fourth quarter of 2026 and inflation 0.8 percentage points higher on average this year,” Amaro said. In this scenario, inflation would exceed 3%, compared with a baseline of 2.2%.

The impact is amplified by gas markets. “Higher gas prices are particularly bad news for the Eurozone,” Amaro said, with the model assuming a temporary near doubling in European gas prices alongside tighter financial conditions and supply chain disruptions.

Title Transfer Facility (TTF) Virtual Trading Point in the Netherlands prices for gas have already risen from around €35MWh pre-war to €51.2MWh as of March 17, but still well off their €300MWh peak in the last energy shock.

If the war expands into the whole region and the disruptions in oil and gas flow turn into the destruction of production facilities, then that would bring broader macroeconomic consequences.

“Another simulation using our economic model with oil prices averaging around $140 per barrel for two months, a temporary near tripling in European gas prices, and additional adverse spillovers takes 1% off Eurozone GDP by the fourth quarter,” Amaro said. Under these conditions, the region would likely experience a mild recession, with “inflation averaging 4% in 2026”.

Despite these risks, Amaro pointed to mitigating factors compared with the last shock.

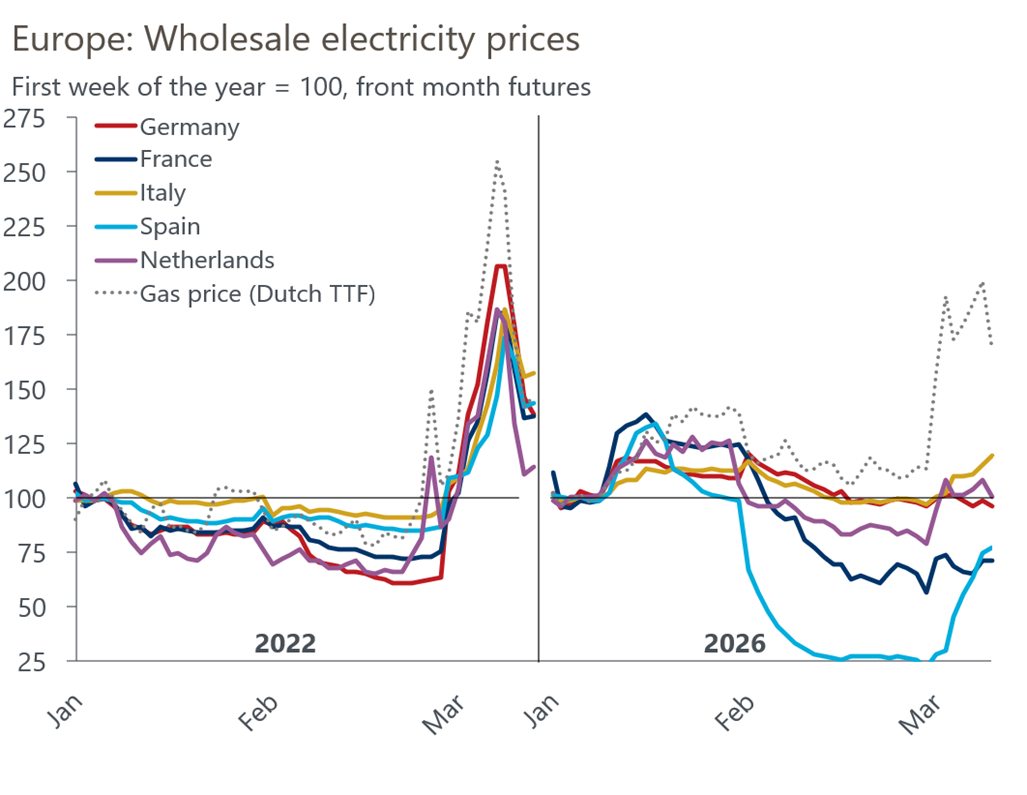

“Wholesale electricity markets appear more resilient to gas prices than four years ago,” he said, highlighting a weaker correlation between gas and power prices. He also expects a faster policy response. “We expect European governments to react more quickly this time,” he said, noting that several countries have already announced support measures and the European Commission is considering options including a potential gas price cap.

However, he cautioned against complacency. “Fuel prices are reacting strongly to the initial increase in oil prices and refined products, meaning a strong immediate impact on consumers should oil prices remain elevated,” Amaro said.

While a worst-case outcome remains unlikely, the balance of risks has shifted. “The risk of a bigger energy shock is rising,” Amaro said.

Unlock premium news, Start your free trial today.