COMMENT: An Iran embargo won't send oil to $200

A chorus of analysts and traders have spent recent weeks warning that oil prices will drift inexorably higher as tanker traffic through the Strait of Hormuz remains disrupted. Robin J Brooks, Former IMF economist, begs to differ — and he has the data to make his case.

"That's not how markets work," Brooks wrote in a blog. "Markets are forward-looking, so — if they expect the Strait to be closed for a significant amount of time — they'll price that in immediately, instead of pricing it slowly as time passes."

He points to what he calls the expectations channel already operating in plain sight: on occasions when President Trump has signalled the conflict is nearing its end, Brent crude has fallen; when the President has struck a more bellicose tone, prices have risen. The mechanism, Brooks argues, is markets constantly revising their estimate of how long the Strait will remain compromised.

"Markets are reasonably efficient and quick about pricing available information. This includes the possibility of an Iran oil embargo. The rise in oil prices likely prices rising odds that Iran's twomn barrels per day go offline."

The practical implication, in Brooks's view, is that an actual embargo — should one be announced — would not produce the violent price spike that many in the market fear. "Some of that's already priced in," he argues. Deploying standard price elasticities of demand, he calculates that shutting in Iran's twomn barrels per day implies an additional $10 rise in Brent. Writing with the benchmark around $114 a barrel, he puts his best estimate for the post-embargo ceiling at roughly $120 — "not much higher."

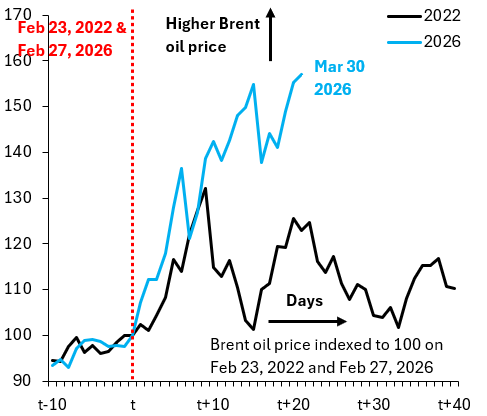

To give a sense of scale, Brooks draws on the aftermath of Russia's 2022 invasion of Ukraine. Russia exports approximately 7mn barrels per day, compared with the 20mn that ordinarily transit the Strait of Hormuz. The current episode is therefore, in his framing, "three times as important for global oil markets" as the Russian invasion — and the price action appears, in his assessment, to reflect that magnitude appropriately.

"The blue line shows the rise in Brent since the start of hostilities — up 60%," he notes. "The black line is the rise in Brent on a similar time scale back in 2022 — up 20%." The ratio, he contends, is broadly consistent with the relative size of each supply shock. That is why, he argues, the more alarming forecasts calling for $150 or even $200 a barrel lack a sound analytical foundation: "Markets are pricing the greater order of magnitude of this shock correctly, so it's far from obvious why Brent should go to $150 or $200."

"I consider these numbers upper bounds to what will happen, because they assume permanent supply disruption, when — in reality — all of us know the midterms mean this conflict can't turn into an open-ended war."

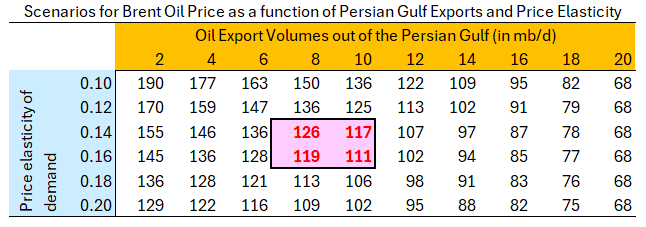

Brooks's modelling uses a matrix of price-elasticity assumptions against scenarios for oil export volumes out of the Persian Gulf. With an elasticity of 0.15 — the mid-point of the range he has encountered in the literature — and Persian Gulf flows running at roughly half their normal capacity, his model places Brent at approximately $114. Layering in a full Iranian embargo pushes that to around $123. He is quick to note, however, that these figures represent upper bounds, predicated on a permanent supply disruption.

Brooks saves his sharpest analytical observation for last. Those who worry that an embargo would deliver an unacceptable oil shock, he contends, are overstating the principal downside risk.

"The single biggest con is that it might spike oil prices," he writes, "and I think that risk is overstated in the popular discourse."

The more consequential concern, in his judgment, is strategic coherence. The current posture — conducting military operations against Iran while simultaneously permitting the oil exports that fund Tehran's budget and, by extension, its allies — represents a form of self-defeating mixed messaging. "It's this mixed messaging that's at the root of why Russia is still able to fight in Ukraine over four years after the invasion," Brooks contends, drawing a direct line between Western energy policy and the durability of the conflict in eastern Europe.

His conclusion is unambiguous: the pros of an embargo outweigh the cons, the oil-price risk is analytically manageable, and the strategic cost of inaction is being systematically underweighted by policymakers and markets alike.