TCHAKAROV: Shockwaves from Tehran in the Caucasus and Central Asia

Crises in geopolitics do not necessarily feature as the main topic of conversation until such time as they begin to impact trade routes, inflation forecasts and central bank decisions. The latest round of crisis surrounding Iran is, however, quickly becoming one of those episodes for the economies of the South Caucasus and Central Asia. Iran borders some of the most important trade routes and oil markets for the countries in the region. Naturally then, the spillover effects of recent developments have already begun to manifest themselves in ways that demand investor attention.

For Armenia in particular, the Iran turmoil zooms in on weak points that have been quietly, yet inexorably, building up in recent years. The implications, of course, extend well beyond Yerevan as rising energy prices are complicating the inflation outlook across the broader Caucasus and Central Asia, forcing policymakers — and investors — to rethink their expectations for the year ahead.

Armenia: the most directly exposed economy

Of the three countries of the South Caucasus region, Armenia is the one most impacted by instability in Iran. In recent years, Iran has emerged as a major trade route for Armenia’s external trade. Currently, 30% of its foreign commerce is conducted through Iran, up from only 18% in 2020. Hence, whenever instability strikes Iran, Armenia is impacted almost at once. The early signs of this impact are already visible in the realm of logistics. The trade route via Iran is now being gradually substituted by Georgia’s Black Sea port city of Poti. While this ensures the continuation of trade flows between Armenia and other countries, this is hardly the best option for Yerevan. The alternative route is longer and more expensive. It takes more time for goods to be delivered to their destination, and Armenia is also becoming more reliant on a single route via Georgia into the West.

Armenia had also hoped to claim a role as a transit hub along the International North-South Transport Corridor, linking Russia and the Caucasus with the Persian Gulf and India. That ambition depends heavily on stable transit through Iran. If Iran becomes a prolonged zone of instability, Armenia risks losing not just current trade efficiency but also a potentially valuable geo-economic opportunity

There is also a longer-term strategic issue at stake. Armenia has attempted to walk a fine line with regards to events within its strategic partner Iran, but remaining neutral has become increasingly difficult. Recent defence cooperation between Armenia and the United States, for example, has resulted in Armenia purchasing V-BAT unmanned aerial systems from the United States for $11mn. This is not something that Tehran can easily overlook in addition to its deep suspicions about the true goals of the TRIPP. Hence, Armenia is increasingly finding itself sandwiched between competing geopolitical objectives at precisely the moment when stability along its southern border matters the most.

How the region is economically linked to Iran

If we look away from geopolitics for a moment, it is instructive to assess how the South Caucasus countries are economically connected to Iran, the Persian Gulf countries and Israel. There are four obvious angles to consider-trade, foreign direct investment (FDI), tourism and remittances:

- Trade — Armenia’s key vulnerability. Trade is by far the most significant economic connection. In 2025, Armenia’s total trade turnover with Iran, the Persian Gulf countries, and Israel was a hefty 11% of GDP. This makes Armenia the country that is most likely to face economic disruption as a result of its relations with these countries. Though Georgia and Azerbaijan also trade with Iran, the Persian Gulf states and Israel, the amount of trade is smaller and, at less than 3% of their GDP for both countries, the severity of economic disruption may not be great.

- Foreign direct investment — Azerbaijan’s soft underbelly. If we look at FDI, however, the situation is a little different. Armenia receives almost 20% of its foreign direct investment from Iran (4.4%) and the Persian Gulf countries (14.8%). As a share of GDP this comes to 7%. Armenia (2.6% of GDP) and Georgia (0.3% of GDP) are less dependent on FDI inflows from these destinations.

- Tourism — Georgia’s hidden weakness. Indeed, Georgia has been witnessing a tourism boom over the past years, achieving record-high foreign exchange income from foreign visitors last year. A significant 20% of Georgia’s visitors come from the affected destinations, including 12.5% from Israel, 4.5% from the Persian Gulf and 2.5% from Iran. At the same time, these flows account for only 2.4% of GDP, pointing to only a relative significance for Tbilisi. Tourism revenues from Iran, Persian Gulf and Israel are less than 1% of GDP for Armenia and Azerbaijan.

- Remittances — a smaller factor. Remittances from Iran, the Gulf states or Israel for the region’s countries are negligible, making up less than 1% of GDP for the South Caucasian economies.

The inflation angle

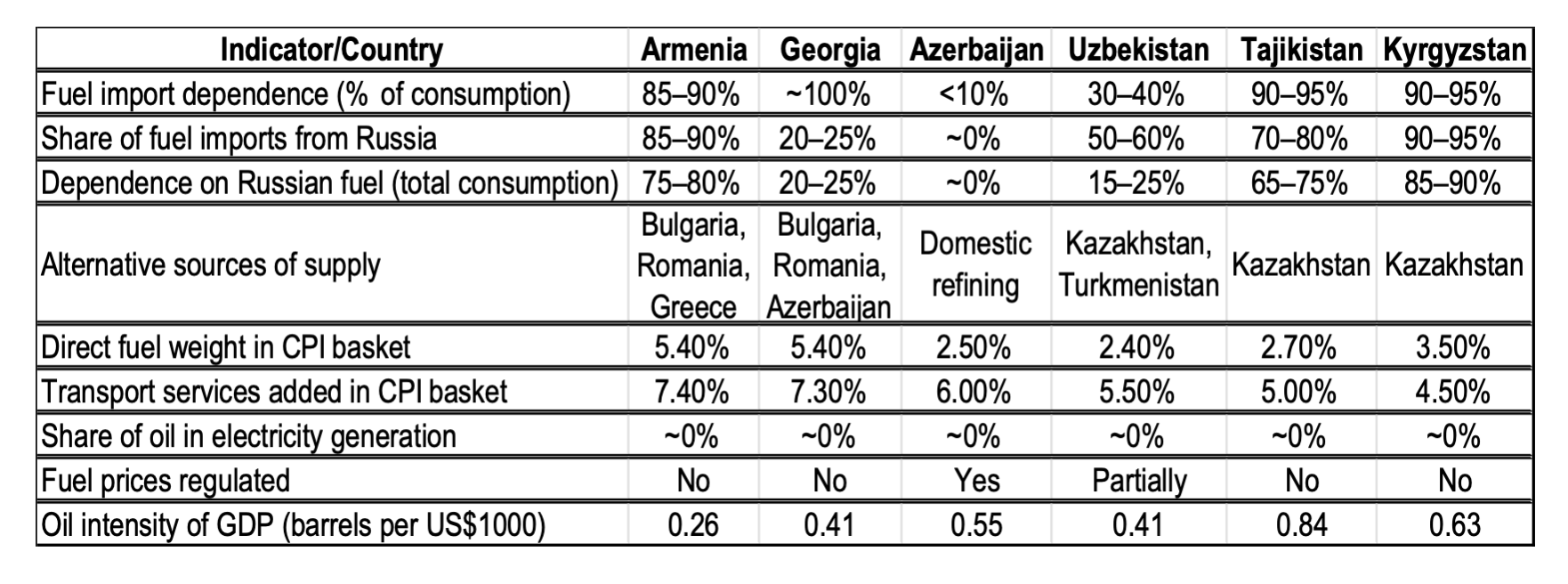

While Armenia’s trade exposure is a key issue, the region faces another problem: rising global energy costs. Earlier this year, it seemed that inflation in the Caucasus and Central Asia had reached a peak in 2025, and that it would gradually decrease in 2026. This assessment was also based on the assumption of continued moderation of global oil prices, but the Iran crisis changes this. Most of the countries in this region, save for Azerbaijan, are net energy importers. Fuel prices have already started to creep up everywhere, with highest increases recorded in Tajikistan and Georgia.

The impact of higher global oil prices will depend on a variety of factors, including dependence on fuel imports, availability of alternative suppliers, weight of fuel/broader energy in the CPI, and degree of domestic control of prices, among others. The direct share of fuels in consumer baskets is not very high, averaging 2.5-5.4%. However, it goes up to 5-7% if we include transportation services.

Even a moderate oil shock could thus materially shift the inflation outlook — and with it, the policy path for interest rates. A 10% increase in oil prices — roughly the adjustment implied by the post-Iran shift in global forecasts — could add about 0.4-0.7 percentage points to headline inflation across the region. That alone is enough to push projected inflation above central-bank targets in several economies, effectively halting the anticipated regional disinflation cycle. For investors, this should translate into a clear re-pricing of rate expectations, with Uzbekistan emerging as the stand-out casualty given that, pre-Iran, the totality of underlying factors were consistent with a more forceful downward move in policy rates this year. The scope for monetary easing in Georgia, and Azerbaijan has also effectively closed, Armenia may now be facing tightening risks, Kyrgyzstan appears set to continue on its ongoing hiking path, while Tajikistan will finally switch from easing to tightening.

The broader energy impact

A simple vulnerability framework I have developed suggests that Kyrgyzstan and Tajikistan are the most exposed to the oil shock, while Azerbaijan is the best insulated. Heavy dependence on imported energy sources, lack of supplier diversification, and higher oil intensity of GDP make the first two Central Asian economies particularly vulnerable to rising energy costs. Azerbaijan is at the opposite end of the spectrum due to domestic refining and administered pump prices. Armenia, Georgia, and Uzbekistan are somewhere in the middle, although the latter is in a slightly better position due to some domestic refining and a lower oil share of the energy mix. The table below summarises the key elements of the impact.

Ivan Tchakarov is partner for the Caucasus and Central Asia at GlobalSource Partners.