Middle East conflict fallout to slow growth, push up inflation in Emerging Europe and Mediterranean region, EBRD says

Rising energy and fertiliser prices triggered by the conflict in the Middle East are expected to push up inflation and dampen economic growth across the European Bank for Reconstruction and Development’s (EBRD’s) regions of operations, the development bank said in a new assessment released on March 26.

In a report titled “Potential economic impact of the conflict in the Middle East,” the bank warned that the economic fallout is already spreading through commodity markets, trade routes and financial systems, with effects likely to persist even after the fighting subsides.

The impact is set to be felt across the EBRD’s region of operations, spanning Emerging Europe, Central Asia, the Southern and Eastern Mediterranean (Semed) and parts of Sub-Saharan Africa, but to be particularly damaging to energy importing and tourism dependent economies.

“The conflict shows how quickly geopolitical shocks can ripple through energy markets, supply chains and financial conditions,” said Beata Javorcik, the EBRD’s chief economist, as quoted in a press release.

“Rising energy prices come at an already challenging time for the European manufacturing sector, while the broader fallout from the conflict is likely to strain government budgets already overstretched by high defence spending in central Europe and elevated debt-servicing costs in the southern and eastern Mediterranean and sub-Saharan Africa. The effects of the conflict are likely to linger beyond the end of hostilities.”

Source: EBRD.

Outlook deteriorates

The EBRD said that continued disruption could have a measurable impact on global and regional growth. “Global growth could be reduced by at least 0.4 percentage point, while inflation could rise by more than 1.5 percentage points” if oil prices remain elevated and supply chain disruptions persist, the report said.

Under such a scenario, “growth forecasts for the EBRD regions could be cut by up to 0.4 percentage point in the Bank’s next outlook.”

The report points to energy markets as the primary transmission channel. Oil prices rose above $100 per barrel in March, while natural gas prices in Europe surged after production disruptions in Qatar.

“Energy prices have increased sharply as a result of recent disruptions to production and transport routes in the Persian Gulf,” the EBRD said. Although current prices remain below historic peaks, the bank warned that markets remain highly sensitive to further shocks. “Short-term demand for energy is relatively inelastic and prices could rise significantly further should disruptions persist.”

The report added that “oil demand in the short run is inelastic and prices might reach US$180 per barrel if Gulf oil remains largely off-market.”

Natural gas markets are also under pressure, particularly in Europe, where storage levels are lower than in recent years. “Gas markets remain tight, with European storage levels significantly below those seen in recent years,” the report said.

Even in the event of a rapid de-escalation, prices are expected to stay elevated, as production of liquified natural gas (LNG) production would take time to resume.

Strain on energy importers

The EBRD highlighted a growing divergence between energy exporters and importers, where the burden will fall disproportionately. Many import-dependent economies already face fiscal constraints.

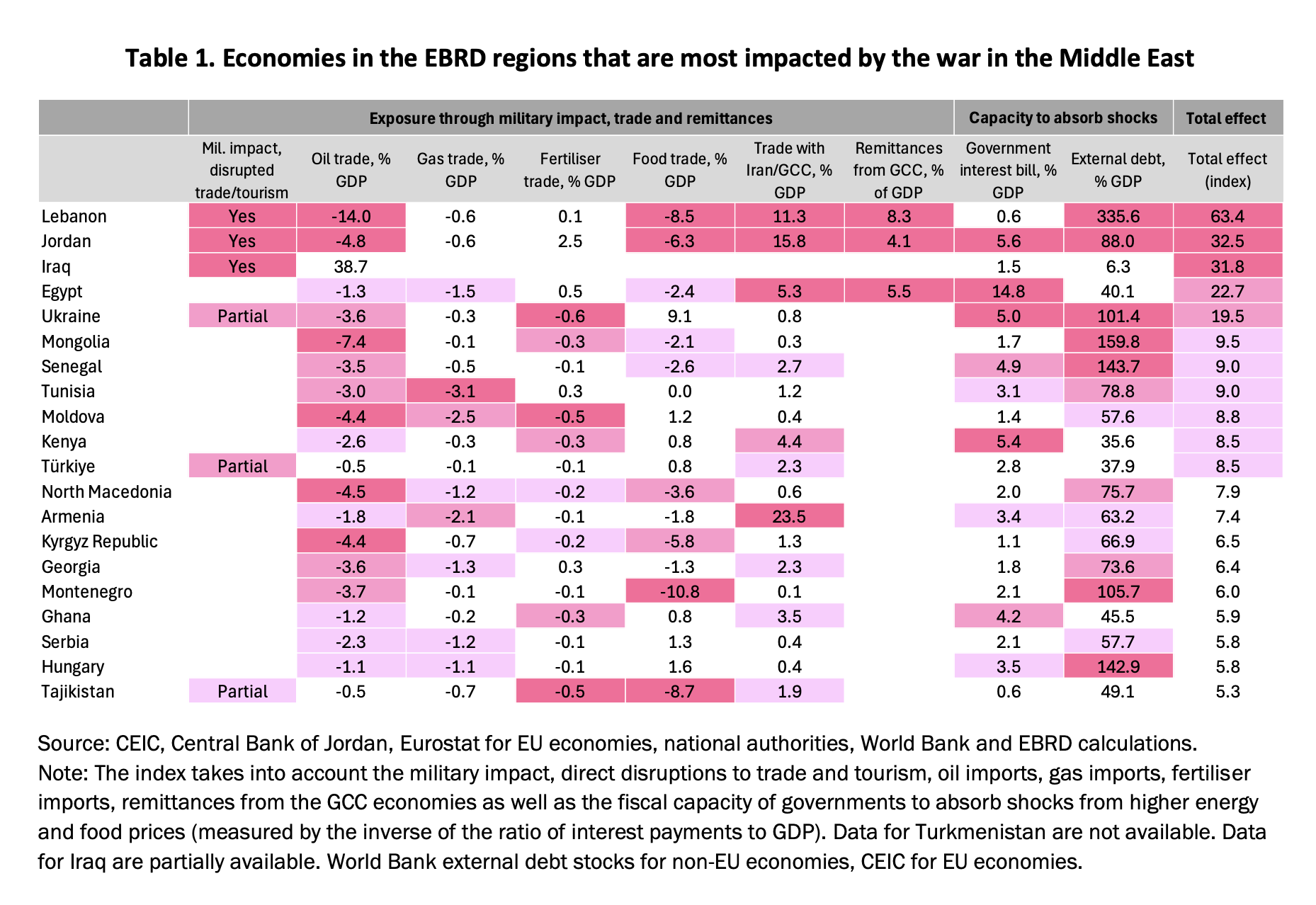

“Economies with high energy, fertiliser and food import dependence, strong links to the Gulf and limited fiscal space are likely to be most affected,” according to the report.

Among the countries identified as particularly exposed are Lebanon, directly involved in the fighting, and Jordan, as well as Egypt, Iraq, Jordan, Kenya, Moldova, Mongolia, North Macedonia, Senegal, Tunisia, Turkey and Ukraine.

The assessment is based on direct disruptions from the conflict, as well as “energy imports, fertiliser and food import needs, remittances from the GCC, and fiscal capacity to cushion rises in the prices of energy and food”.

The report also warned of knock-on effects in agriculture, driven by rising fertiliser costs, as around 25-35% of global trade in the raw materials for fertilisers passes through the Strait of Hormuz, creating a direct link between the conflict and global food prices.

Countries with strong reliance on Gulf imports are particularly exposed with the EBRD signing out Kenya and Turkey, which receive 31% and 13% of fertiliser imports, respectively, from the GCC.

While many economies face headwinds, commodity exporters are benefiting from higher prices. “In Russia… every US$ 10 per barrel increase in the oil price is estimated to be associated with a windfall in revenues… equivalent to 1.5 percentage points of 2025 GDP.”

The report added that the war has also created opportunities for Russian oil sales. “The war has also enabled Russia to clear the backlog of oil at sea looking for buyers and reportedly sell this backlog… at a premium to the Brent oil price.”

Supply chains under pressure

Beyond agriculture, disruptions to Gulf trade routes are affecting a range of industrial inputs. “If trade to / from the GCC continues to be disrupted, temporary shortages and upward price pressures for aluminium, sulphur, helium (for semi-conductors), petrochemicals, plastics and other goods may intensify in the short term, propagating through supply chains and adding to global inflationary pressures,” the report said.

While direct trade with Iran is limited, and concentrated in the Caucasus region, the EBRD noted that links with Gulf economies are far more significant.

The report identified tourism and remittances as additional channels through which the conflict is affecting economies.

Meanwhile, financial inflows from migrant workers may also weaken. “Remittances from GCC countries – an important source of income for economies including Lebanon, Jordan and Egypt – may come under pressure.”

The economic impact is being compounded by tightening financial conditions, says the report, noting that bond yields are rising in the southern and eastern Mediterranean region and in Turkey.

So far, the situation has remained manageable, but risks are rising. “Capital outflows from some economies have so far remained manageable, but could intensify if global financial conditions deteriorate further,” the EBRD said.

“The extent to which economies can cushion the terms-of-trade shocks will depend on their fiscal and external buffers.”

Countries with limited fiscal space may struggle to shield households and businesses from rising costs. “The direct negative effects on GDP growth via energy costs, the price of fertilisers and food staples, disruptions to supply chains, tourism and remittances from the GCC will be compounded by higher inflation, greater pressures on government budgets and tighter financing conditions in response to rising inflation.”

Longer-term structural shifts

Looking beyond the immediate impact, the EBRD said the conflict could accelerate structural changes in the global economy.

“In the longer term, the conflict may reinforce the importance of energy security and accelerate the fragmentation of global trade, particularly in energy and critical raw materials.”

Recent geopolitical tensions have already exposed vulnerabilities in global energy systems. However, the report noted that global dependence on hydrocarbons is lower than in previous decades, limiting the scale of the shock compared to the 1970s.

The EBRD said the overall economic impact will depend on how long the conflict lasts and how severely energy infrastructure is affected.

“The overall economic impact of the war will be determined by the duration of the conflict and the extent of the damage to energy infrastructure.”

However, even in the best-case scenario, the consequences are likely to be prolonged. “The impact will likely linger beyond the end to hostilities,” the EBRD warned.

Unlock premium news, Start your free trial today.