BEYOND THE BOSPORUS: What no crisis!? Turkey is so far riding out economic shocks of the Iran war

Newsrooms with an eye on Turkey have been lately struggling to believe that since the end-of-February onset of ‘Gulf War III’, there’s so far been hardly a trickle of articles suggesting big crises are taking hold in its economy.

Turkey in recent years has many times proven its ability to descend into a crisis without the need for an external shock to make it happen. Now we have huge disruption from outside, yet no crisis.

The US/Israeli war on Iran and consequent impacts on Gulf energy exports have yet to deal a significant blow to Turkey’s energy supplies, while on the markets, the country has not faced any truly painful portfolio outflows.

Oil and gas factors

Turkey sources around 10% of its oil imports via the Hormuz Strait, currently subject to selective blocking by Iran. Also, around 10-15% of the country’s natural gas is drawn from Iran’s largest gas field, South Pars in the Gulf. Qatari liquefied natural gas (LNG), however, does not make up a significant share in Turkey’s gas supplies.

Gas from Iran

On both March 24 and March 25, Turkey’s energy minister, Alparslan Bayraktar, denied a Bloomberg report that suggested Iran had halted its piped supplies of gas to Turkey. He did not, however, dismiss the possibility that such a suspension could be ahead.

Nevertheless, if the gas flow from Iran is suspended, Turkey should be able to maintain its gas supplies at a sufficient level. State companies have recently signed sizeable LNG contracts with US suppliers.

The real problem centred on the gas flow from Iran is actually related to Turkey’s domestic pipeline network. The country is unable to pump gas from its western network to eastern provinces that use Iranian gas.

However, the eastern network has a connection to the entry point of the Trans-Anatolian Natural Gas Pipeline, or TANAP, which brings in Azerbaijani gas. It can also make use of a floating storage and regasification unit (FSRU), which converts LNG shipped to Dortyol, in southernmost province Hatay, into consumable gas.

Thus, it seems the gas supply picture in the eastern provinces is manageable and, should there be shortages, it is notable that Turkey’s economy would not be hit particularly hard as the share in the country’s economic activity of these provinces is low.

$20bn of war-time portfolio outflows in first two weeks

Looking at the currency side, Turkey faced $13bn worth of carry trade outflows and the exit of $6bn from domestic government bonds and equities in the first two weeks of the war (between Friday February 27 and Friday March 13).

In addition to the portfolio outflows, $1bn worth of deposits were withdrawn from the banking system in the same period.

The required central bank intervention in response to these exits combined has been estimated at $20bn. Turkey’s central bank does not officially announce its currency market interventions, though, and the recent fluctuations in gold prices make it harder to estimate their exact volume.

| Portfolio outflows from Turkey | |||||||||||

| Carry Trade Flows to Turkey (estimate) | Lira papers | Total | |||||||||

| million USD | Turkish Banks Off-Balance Sheet FX Position | Turkish Central Bank's Total Swap Stock with Local Banks | Lira-settled FX Frowards | Turkish Central Bank's Net FX Derivatives Stock with Local Banks | Turkish Banks' Swap Stock with Foreign Counterparts (estimate) | Carry Trade Flows (estimate) | Cumulative Flow Carry | Domestic Government Bonds Weekly Flow | Equity Weekly Flow | Carry plus Lira Papers | Cumulative Total |

| Feb 27 | 55,649 | -3,417 | 0 | -3,417 | 59,066 | ||||||

| Mar 6 | 51,183 | -2,646 | 507 | -2,139 | 53,322 | -5,744 | -1,726 | -756 | -8,225 | ||

| Mar 13 | 45,517 | -1,695 | 804 | -891 | 46,408 | -6,914 | -12,658 | -2,878 | -322 | -10,114 | -18,339 |

Table: Portfolio outflows from Turkey.

$50bn+ in liquid firepower

Coupled with the sharp decline in gold prices, the Turkish central bank’s reserves have fallen. However, the fallout has not got beyond manageable. For the sake of speculation, another $20bn of portfolio outflows looks entirely manageable.

Observers are busy assessing the liquid FX reserves held by the authority (meaning those available to use in currency market interventions).

Tweets: Estimating the central bank’s firepower.

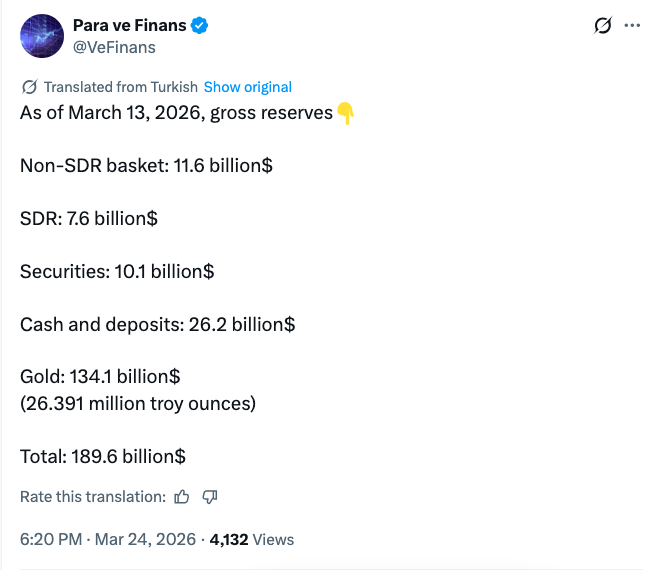

As of March 13, the central bank reported $190bn in gross reserves. Around $134bn was in gold, suggesting 26mn troy ounces or 821 tonnes of gold.

Of the other $56bn in FX reserves, $8bn was in special drawing rights (SDR), the IMF’s currency. In other words, that part of the reserves is not liquid. Another $12bn of the reserves is in currencies that are not part of the IMF’s SDR basket. This capital stems from swap agreements with countries such as China.

The calculations show the central bank has $26bn worth of firepower in cash (printed money) and deposits. This is the most liquid part of what it boasts. Additionally, the authority has $10bn in securities, mainly US Treasuries. This is also convertible to cash at any time. We arrive at a total of $36bn that is available to use.

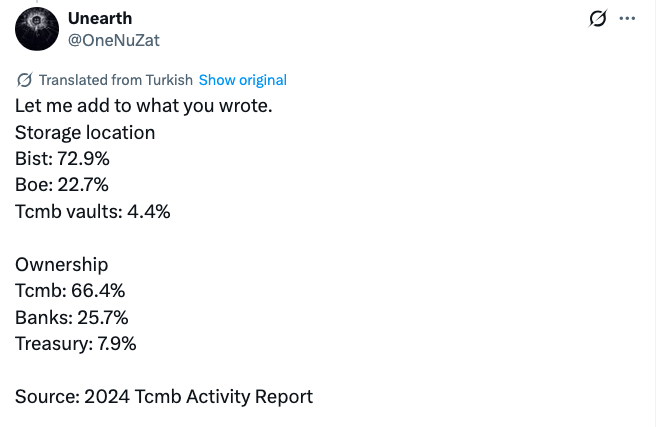

According to the latest available data (provided in the central bank’s annual report released in April), the regulator has placed around 20-25% of its gold with the Bank of England. This means that approximately $20-30bn of gold is available to convert for use should that be required.

On March 24, Bloomberg quoted unnamed people familiar with the matter as saying that the central bank went into discussions on conducting gold-for-FX swap transactions on the London market.

Government-run players active in eurobond and loan markets

In the event of sustained pressure being exerted on the reserves, the access of Turkish borrowers to the eurobond and loan markets would be critical. When the US and Israel mounted their surprise attack on Iran on February 28, igniting the current conflict, eurobond sales and the flow of new loan deals stopped.

On March 24, government-run telco Turkcell (TCELL) announced a $1bn syndicated murabaha loan deal and government-run Halkbank (HALKB) announced a $210mn subordinated AT1 eurobond.

Whether other borrowers will retain their access to the international debt markets will be watched closely.

Oil price shock hits inflation

Booming oil prices have, meanwhile, been hitting Turkey’s already elevated inflation. However, no one, excepting the media, had any faith that the country’s government was on course to solve the chronic Turkish inflation problem.

Rising inflation in itself does not signify a crisis.

Real sector troubles

Turkey’s plastics industry has already felt a doubling of costs. Brittle tourism demand amid the missiles flying across the Middle East (just three have made it to Turkish airspace. They were shot down by Nato, and Iran denied firing them) is also a source of stress.

Real risk

The real risk is that Turkey could at any time in some way be drawn into a widening, spiralling conflict.

Unlock premium news, Start your free trial today.