Iran war accelerates Chinese US treasure bill sell off

The war in Iran has triggered a potential step change in the rate that China is selling off its US Treasury bill holdings. T-bill holdings are a good barometer for geopolitical tensions and the rate that China and BRICS countries were selling had already accelerated before the Iran war.

As the Middle East conflict escalates, it is fuelling tensions as it hits oil deliveries to Asia particularly hard, and the selling of T-bills appears to have accelerated again. Holdings have fallen to their lowest level since September 2008, in what could be a possible prelude to China launching an attack on Taiwan, Beijing follows the same path as Russia.

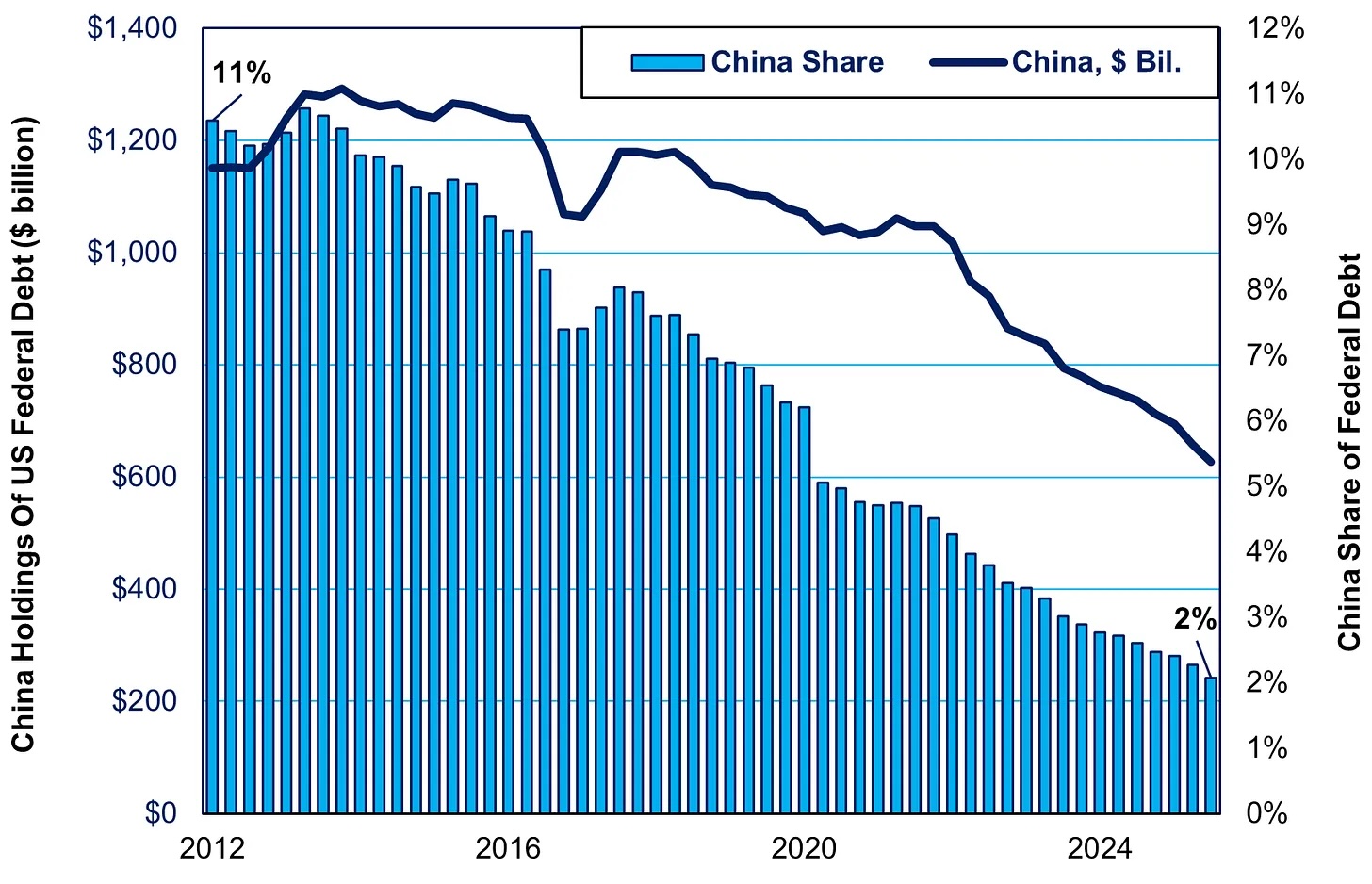

Data from the US Department of the Treasury show China’s holdings declined to $633.4bn from $682.6bn in November 2025, and an all-time peak of $1.316 trillion in November 2013 – a fall of $50bn in four months. That is not as extreme as the Russian sell off in 2018, when the Ministry of Finance (MinFin) dumped $80bn in two months and exited the market.

However, Chinese selling followed a string of notable drawdowns, including a $120bn reduction in June 2019 during the trade war with the first Trump administration and a $176bn decline by May 2022 after the US weaponised the dollar with the Russian sanctions. In 2012, Chinese entities owned 11% of Treasury bonds; today, it’s just 2%

Beijing has also ordered all its commercial banks to sell their T-bill holdings as the Chinese withdrawal from US dollar denominated assets accelerates. It is not clear how large these holdings are, but market participants estimate the value to be between $70bn and $200bn. If the amount is at the lower end of the range, dumping those bonds will have little effect but if at the upper end of the range then selling $200bn worth of treasury bills would move into a “step event” territory.

Potential step event

As the IntelliNews Lambda analysis showed, holdings of US Treasury bills are a good barometer for the geopolitical climate. China’s T-bill holdings have been halved from its peak and accelerated in the last year.

There have been three periods of selling driven first by rising tensions over trade relations during US president Donald Trump's first term in office. The next important point came the American decision to weaponize the dollar in 2022 by seizing some $300bn of Russian central bank reserves when the rate of selling increased. The most recent sell off, and the most aggressive, began in April last year after the Trump administration unveiled its Liberation Day sanctions scheme and tried to impose a rate of over 100% on China – an effort Beijing saw off by threatening to throttle the exports of rare earth metals (REMs).

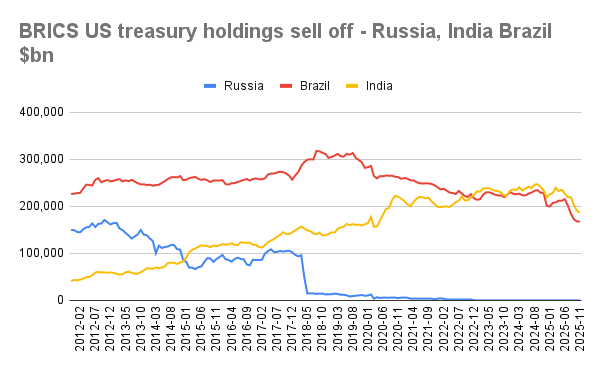

The other BRICS nations have reacted to the Liberation Day tariffs and suddenly begun to dump US dollar denominated assets. Brazil has followed China in gradually reducing its holdings in recent years, but India reversed an accumulation and started selling T-bills heavily since Trump doubled tariffs on India in August for buying Russian oil.

The war in Iran could turn out to be a potential game changing “step change” political event, a singularity that leads to the total exit from the US treasury market. That may also be a prelude to China attempting to take over Taiwan by force, if Beijing follows the Moscow precedent.

In Russia’s case, the key event according to IntelliNews Lambda’s analysis, occurred in April 2018 when the US Treasury Department issued an oligarch sanctions list that included all of Russia's oligarchs, simply copied from the Forbes rich list that year, and actually imposed sanctions on metals and power tycoon Oleg Deripaska.

That produced a radical change in policy and triggered the dumping of the remaining $80bn worth of treasury bills in the space of two months taking the Kremlin’s holding down to next to nothing.

At the time financial analysts in the US dismissed this event as simply the Central Bank of Russia (CBR) readjusting its portfolio from T-bills to gold and missed the political significance of the selling. In retrospect, it appears that exiting completely from US dollar denominated assets was another preparatory step for war as it effectively made Russia sanctions proof. At the same time the central bank increased the share of gold in its reserve mix, which today accounts for half of all of Russia’s international reserves. The CBR no longer holds any dollars or European currencies in its basket, but has massively increased its yuan holdings as part of the yuanization of the Russian economy. The Ministry of Finance also reduced its external debt so today Russia has a mere 15% of GDP in debt - the lowest level of any major economy in the world. It can cover its obligations dollar-for-dollar with the cash that remains in its international reserves.

Now it appears that Beijing is carrying out a very similar operation. It has ordered its banks to reduce their exposure to treasury holdings and at the same time massively and rapidly ramped up its gold holdings. Drawing a parallel with the Russian experience, Beijing is putting itself into a similar position, where it will become increasingly difficult to sanction Beijing if it moves on Taiwan.

Military action against Taiwan is not guaranteed, as the sell off of T-bills could simply be in anticipation of a scaling up of geopolitical tensions between Beijing and Washington related to the Iran war. The Trump administration clearly would like to take control of the Strait of Hormuz, which would give it the power to throttle energy exports to Asia, 90% of which go to China, as part of Trump’s “energy dominance” policy. The US has already cut off oil exports to China from Venezuela since the decapitation of the Maduro regime in January.

However, as the Iran war increasingly goes against the US forces and Trump finds himself immersed in a military imbroglio that has burnt through much of the US stockpile of sophisticated missiles, it has become increasingly clear that America has armed itself for the wrong war. It is not capable of countering Chinese aggression in the Indo-Pacific region as well as in the European and Middle Eastern theatres. If Beijing wants to strike, now is the time to do it.

Banks ordered to sell T-bills

The government has ordered its commercial banks to sell their remaining treasury bill holdings in a move that some analysts are calling a preparation for “China’s exit from petrodollar” system.

Chinese regulators already instructed banks to curb exposure to US Treasuries in February. The directive applies only to private banks, not to the government, which owns the majority of US Treasury debt.

For decades the international oil business has been built around settlements in dollars. That has created what has been dubbed the petrodollar system whereby countries everywhere have to hold dollars in their reserves in order to pay for oil.

One of the consequences of the Iran war is that currently the oil exiting from the Strait of Hormuz under the permits-for-passage system is being paid for in currencies other than the dollar -predominantly Chinese yuan and cryptocurrency.

China has been pressuring its trade partners to swap the dollar for the yuan in mutual trade settlements. At least three countries in Africa either converted or are considering converting their own China-linked loans into the yuan to help save on interest payments. In addition, one more has now joined China's Cross-Border Interbank Payment System (CIPS), reports Capital Economics.

In February, Chinese President Xi Jinping called for the yuan to become a global reserve currency and the Chinese yuan has quadrupled its share as the currency of choice to settle global trade deals, increasing its share from just under 2% in 2020 to over 8% by early 2025, according to data from SWIFT. Likewise, Russia now settles almost all of its mutual trade deals in national currencies.

In a sign of changes underway in the energy markets, gold overtook the dollar in reserve baskets around the world for the first time last month, Bloomberg reports. Gold now accounts for 24% of global central bank reserves, compared with 21% for US government debt, according to the data cited. The change represents a sharp reversal from the final quarter of 2015, when Treasuries made up 33% of reserves and gold just 9%.

If Tehran retains control of the Strait of Hormuz after the war then a significant share of the international oil business will no longer be using the dollar and Beijing will have taken another step closer to establishing the Chinese currency as a global reserve currency.

Economists have pointed out that if the dollar loses its reserve currency status that will create enormous headaches for the US government as the borrowing costs to refinance its gigantic $37 trillion debt will become more expensive. Since the beginning of this year interest payments on this debt have overtaken the budget expenditure on defence.

It remains unclear as to what share of US T-bills are held by China’s commercial banks. The majority of China’s Treasury holdings are widely believed to be controlled by official sector institutions, primarily the State Administration of Foreign Exchange (SAFE), which operates under the People’s Bank of China (PBoC). Market estimates believe that roughly 70–90% of China’s reported Treasury holdings are linked to official reserves, so if all the commercial banks dump their holdings that would amount to approximately $70bn-$200bn of selling – not enough to be a step event at the lower end of the range, but equal to a third of all holdings at the upper end of the range that should start alarm bells ringing.

Unlock premium news, Start your free trial today.