A long Iran war will lead to severe shortages, says Oxford Economics

A sustained escalation of the US/Israel–Iran conflict could push global oil markets beyond a price shock into severe physical shortages, with rationing, supply chain disruption and recessionary pressures becoming increasingly likely, according to a note from Oxford Economics.

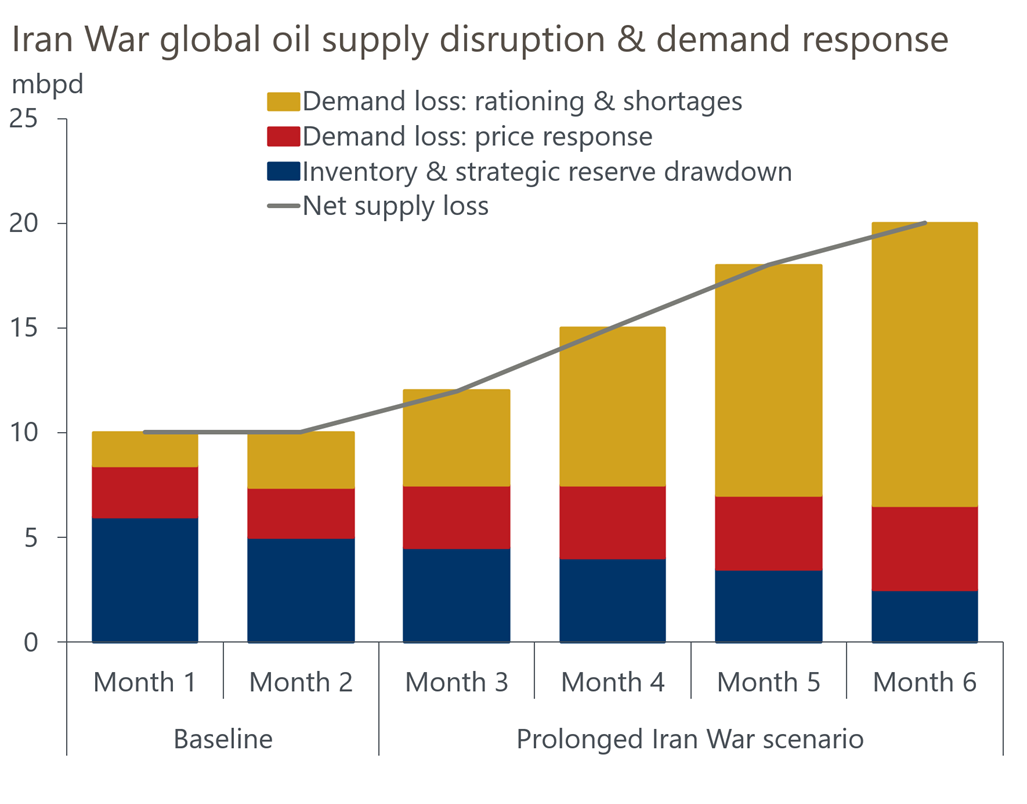

The closure of the Strait of Hormuz has already removed around 10mn barrels per day (mbpd) of oil from global supply—roughly 10% of pre-conflict demand of 104mbpd—even after partial rerouting through Saudi and UAE pipelines. That is going to be hard to replace.

“The deficit can only be closed through three channels: higher prices, inventory drawdowns and, ultimately, rationing,” Oxford Economics said, warning that “the longer the disruption lasts, the more the adjustment shifts into rationing—the most economically destructive outcome”.

Short-run oil demand remains highly inelastic

Short-run oil demand remains highly inelastic

Oxford Economics estimates that a 79% rise in Brent crude prices has reduced global oil demand by just 2.4mbpd, reflecting a short-run price elasticity of approximately -0.03.

“For every 1% increase in price, consumption falls by just 0.03%,” the report notes, adding that “very large price increases only reduce demand modestly”.

The adjustment is uneven across products. Gasoline demand, based on a 95% wholesale price increase, has fallen by around 0.8mbpd from a pre-conflict base of 27mbpd. Diesel, despite a 99% price rise and a similar elasticity, has also declined by only 0.8mbpd from 28mbpd. Jet fuel, with a higher elasticity of -0.05 and a 117% price increase, has seen a 0.5mbpd reduction from 8mbpd of demand.

“Diesel is the biggest issue,” the analysis states. “Its demand underpins freight, agriculture, construction and industrial activity, and these sectors cannot easily switch fuels or cease operations.” As a result, “diesel demand falls relatively little through price alone, which is precisely why shortages are so economically damaging”.

Fuel oil and bunker fuel, with elasticity of -0.01, have seen minimal adjustment despite a 104% price rise, while petrochemicals and other uses account for a 0.3mbpd reduction. “Price does not reduce demand evenly,” Oxford Economics observes, noting that cuts are concentrated in more discretionary segments such as aviation.

|

Short-run oil demand destruction |

||||

|

Product |

Short-run price elasticity |

Pre-conflict demand (mbpd) |

Wholesale price change |

Demand reduction (mbpd) |

|

Gasoline |

-0.03 |

27 |

95% |

0.8 |

|

Diesel |

-0.03 |

28 |

99% |

0.8 |

|

Jet fuel |

-0.05 |

8 |

117% |

0.5 |

|

Fuel oil/ bunker |

-0.01 |

7 |

104% |

0.1 |

|

Petrochemicals/ other |

-0.02 |

27 |

60% |

0.3 |

|

Crude |

-0.03 |

104 |

78% |

2.4 |

|

Source: Oxford Economics, Haver Analytics, IEA |

||||

Inventories and strategic reserves offer limited relief

Inventory drawdowns are currently absorbing much of the shock. Global oil inventories stood at over 8.2bn barrels in January, according to the International Energy Agency, and a coordinated release of 400mn barrels—the largest in its history—has been initiated.

“In practice, not all of that stock is available,” the report cautions. “What matters is not just the volume, but how quickly it can be refined and transported into usable supply.”

The IEA has already called for all-time record reserves release of 400mn barrels of oil from strategic reserves. Against a 10mbpd deficit, the IEA release equates to “only one to two months of lost supply in volume terms”, with a realistic flow contribution closer to 2–3mbpd. Reserves were always designed to deal with temporary disruptions, not a long-term reduction in production.

Structural mismatches further limit effectiveness. “Most strategic reserves are crude, not refined products, and much of the lost Gulf crude is heavy and sour,” the analysis notes. “Releasing lighter crude does not fully address shortages in middle distillates such as diesel and jet fuel.”

As a result, “inventories buy time rather than solve the problem”, delaying but not preventing the onset of physical shortages.

Rationing emerges as the central economic risk

Even after accounting for price-driven demand destruction and inventory releases, Oxford Economics estimates a current shortfall of around 2mbpd—approximately 2% of global demand. In a prolonged conflict scenario, where disruption extends for six months and expands to include attacks on Red Sea shipping and Gulf infrastructure, the gap could widen to around 13mbpd.

“That represents an unprecedented shortage of roughly 12–13% of consumption,” the report states. “At this point, demand falls not because consumers choose to use less, but because fuel is not reliably available.”

Rationing access to fuel has already started. Since the start of the war a growing number of governments are turning to fuel rationing and mandatory purchase limits to conserve supplies and head off shortages, Newsweek reports. But the queues outside petrol stations have already started to grow. In India there has already been a riot at the petrol pumps that saw several people die in the crowd crush.

Sri Lanka: Nationwide fuel rationing reinstated through a QR-code-based National Fuel Pass, with strict weekly caps on petrol and diesel for private vehicles and higher but still limited allocations for essential services.

Myanmar: Odd-even licence plate system introduced, restricting fuel purchases on alternating days to manage acute diesel shortages under government-controlled distribution.

Cambodia: Around one-third of petrol stations shut, creating de facto rationing by limiting access rather than imposing formal purchase quotas.

Slovenia: First EU country to introduce formal fuel rationing, capping private motorists at 50 litres per period and businesses and farmers at 200 litres, amid distribution bottlenecks and fuel tourism pressures.

Bangladesh: Binding fuel rationing measures imposed nationwide as part of emergency efforts to manage limited reserves, with restrictions varying by region and fuel type.

Indonesia: Mandatory fuel purchase limits introduced alongside work-from-home rules for civil servants, with private vehicles capped at 50 litres per day and exemptions for essential sectors.

Philippines: Emergency energy measures implemented, including reduced transport services, but no fixed fuel rationing quotas at the pump.

Egypt: Restrictions placed on non-essential government travel as part of energy conservation efforts, without direct fuel rationing for consumers.

China: Fuel export bans and price controls introduced to protect domestic supply, but no formal consumer-level rationing measures in place.

There are several other countries where shortages have already appeared, but the government has yet to act to limit access to fuel.

India: Localised fuel shortages and market stress, but the government has yet to impose rationing and is relying on administrative controls and supply management measures.. There are reports of petrol stations running dry, panic buying, and black markets for LPG.

Pakistan: Severe fuel supply pressures have led to intermittent shortages, reduced operating hours at petrol stations, and prioritisation of fuel for essential sectors. While no formal nationwide rationing system is in place, administrative controls and import constraints are effectively limiting access.

Vietnam: Fuel shortages have disrupted transport and aviation, with reports of flight cancellations linked to jet fuel constraints. The government is seeking emergency crude supplies and tightening distribution, but has not introduced formal consumer rationing.

Thailand: Widespread shortages have led to petrol stations running dry in some areas and government intervention through price caps and export bans. While not framed as rationing, these measures are constraining availability.

Laos: Heavy reliance on imported fuel and limited foreign currency reserves have led to recurring shortages and long queues at petrol stations. Authorities are managing supply through distribution controls rather than formal quotas.

Nepal: Supply disruptions linked to regional constraints have resulted in sporadic shortages and prioritisation of essential services, without a formal rationing framework.

South Africa: Logistics bottlenecks and refinery outages have tightened fuel supply, with some regions experiencing temporary shortages. The government has relied on market and logistical adjustments rather than rationing.

Kenya: Currency weakness and high import costs have strained fuel supply chains, leading to delays and occasional shortages, though without formal rationing policies.

The shift from price adjustment to rationing marks a critical threshold. “This is where the real economic damage sits,” Oxford Economics says. Supply chain breakdowns and constrained financing for fuel purchases will hurt economic activity and could trigger a global recession, with world GDP growth slowing to 1.4% in 2026.

Diesel shortages amplify system-wide disruption

Diesel supplies are the biggest problem. “It powers road freight, agricultural machinery, construction equipment and a large share of industrial activity,” Oxford Economics says. “When diesel supply is physically constrained, the impact spreads through freight costs, food production and industrial output simultaneously.”

Diesel shortages are already hurting the most vulnerable economies mostly in Asia. The Philippines has declared a national energy emergency and introduced a four-day working week, while Pakistan has implemented similar measures in the public sector. Bangladesh has imposed fuel purchase caps and closed universities, and Myanmar has introduced alternating driving days.

Thailand has capped diesel prices and banned fuel exports, while Vietnam is seeking emergency crude supplies from outside the Gulf. “Adjustment has moved beyond price into access restriction,” Oxford Economics notes, pointing to panic buying, black markets for liquefied petroleum gas in India, the tightening credit conditions among fuel traders and an explosion of theft, siphoning off fuel from the tanks of parked cars. “The pressures are cascading across borders.”

Export restrictions by China and Thailand are worsening shortages in neighbouring economies, while Vietnam Airlines has cancelled flights due to jet fuel shortages. “Each country’s attempt to protect its own market makes the regional picture worse.”

Regional divergence shapes the global impact

The severity of the shock varies significantly by region. “North America is the most insulated,” Oxford Economics says, thanks to its status as a net fuel exporter, ample inventories and flexible refining capacity. However, it warns that “the US remains highly oil-intensive, so higher pump prices will still feed into inflation and household costs”. Prices at the pump for petrol crossed $4 this week, and the cost of diesel has already doubled, which is going to cause US President Donald Trump political problems.

Europe occupies a middle ground. “It has more storage and policy capacity than many importers, but remains exposed, particularly to prolonged disruption in middle distillates,” the analysis notes. Efforts to shield consumers from price increases may also “slow demand adjustment and accelerate stock drawdown”.

China is also relatively insulated due to domestic production of around 4mbpd, large reserves of some 1.2mn barrels, a large coal-fired power reserve and nuclear power back-up and state control over its energy system, but is likely to prioritise domestic supply. “Fuel export restrictions from China would exacerbate shortages elsewhere in Asia,” the report says.

Emerging economies across Asia Pacific and sub-Saharan Africa remain the most vulnerable as they are the most heavily dependent on exports from the Gulf.

“They combine heavy import dependence with limited inventories and weaker fiscal capacity,” Oxford Economics says, highlighting risks across the Philippines, Vietnam, Thailand, Bangladesh and Pakistan.

Gas markets remain more resilient globally

In contrast to oil, natural gas markets are less likely to experience global shortages. The loss of Qatari liquefied natural gas—around 90mn tonnes of oil equivalent, or 20% of global LNG trade—amounts to only about 3% of total global gas consumption of 3,524mn tonnes of oil equivalent.

“Gas demand is much more price-responsive, with short-run elasticity of around -0.07,” Oxford Economics calculates. A projected 33% increase in global gas prices implies around 80mn tonnes of oil equivalent in demand destruction, broadly offsetting the lost supply.

“Power systems can switch from gas to coal relatively quickly, which provides an effective adjustment channel,” Oxford Economics explains. However, flexibility is limited outside the power sector, particularly for residential use and industrial feedstocks.

“Countries with coal switching capacity can adjust, but those reliant on Qatari LNG with limited alternatives—such as Bangladesh and Pakistan—face a physical supply shock,” the report concludes. Europe, meanwhile, “can balance the market globally but remains exposed due to low storage and a challenging gas refill season”.

“Oil is different,” the analysis concludes. “Inventories are still being drawn down, and the disruption could intensify further, making the risk of severe shortage materially higher over time.”

Unlock premium news, Start your free trial today.

_6.jpg)