Cost of living shock deepens as energy crisis hits G7 spending – Oxford Economics

A surge in energy prices following the escalation of the Iran conflict is intensifying the cost-of-living crisis across the G7, dragging consumer spending growth to its weakest level since 2022, according to a note by Ryan Sweet, Chief Global Economist at Oxford Economics.

Rising prices were already eating into incomes and making life more difficult before the war in Iran broke out, but as the spike in energy prices ripples out around the world, the cost-of-living crisis is getting worse.

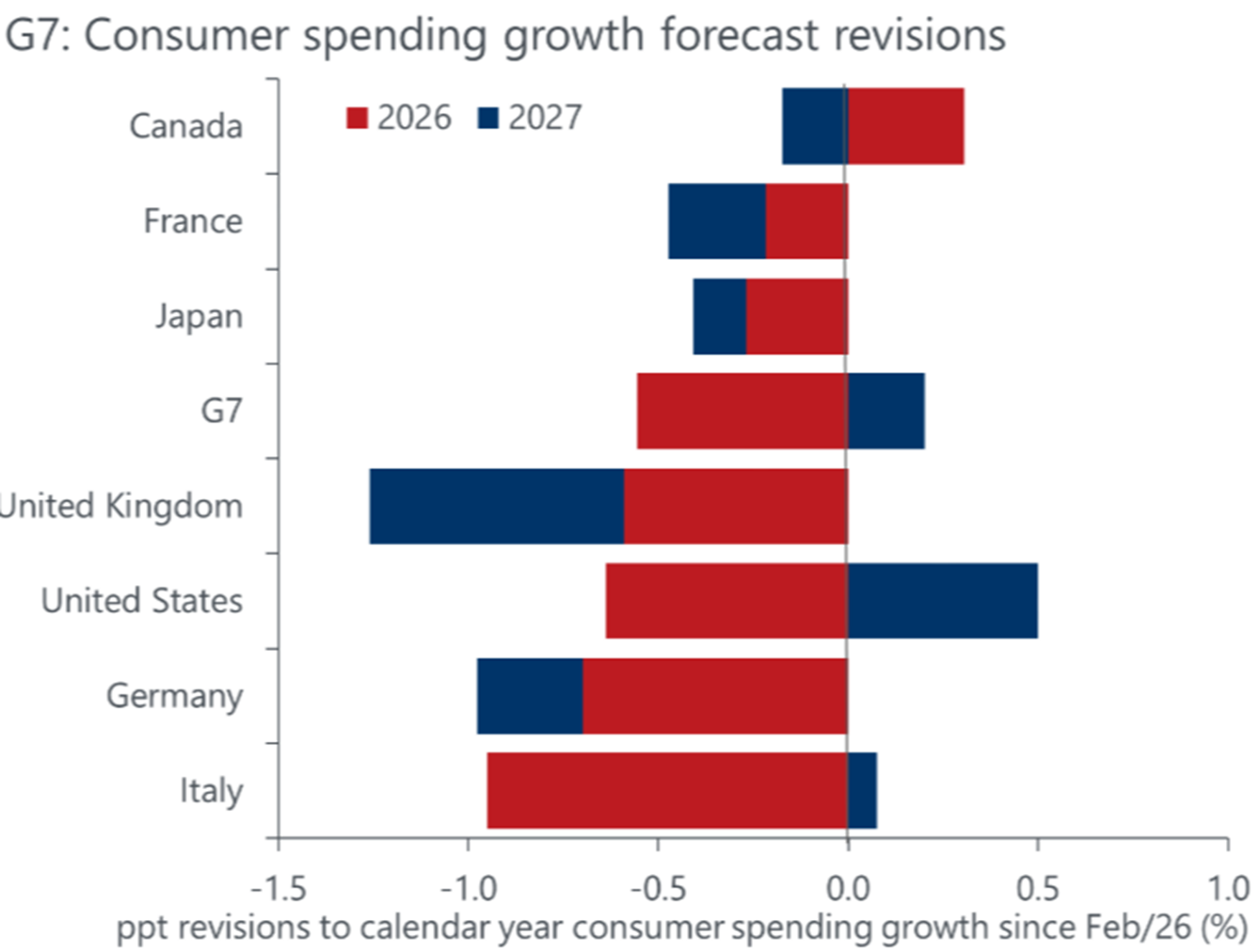

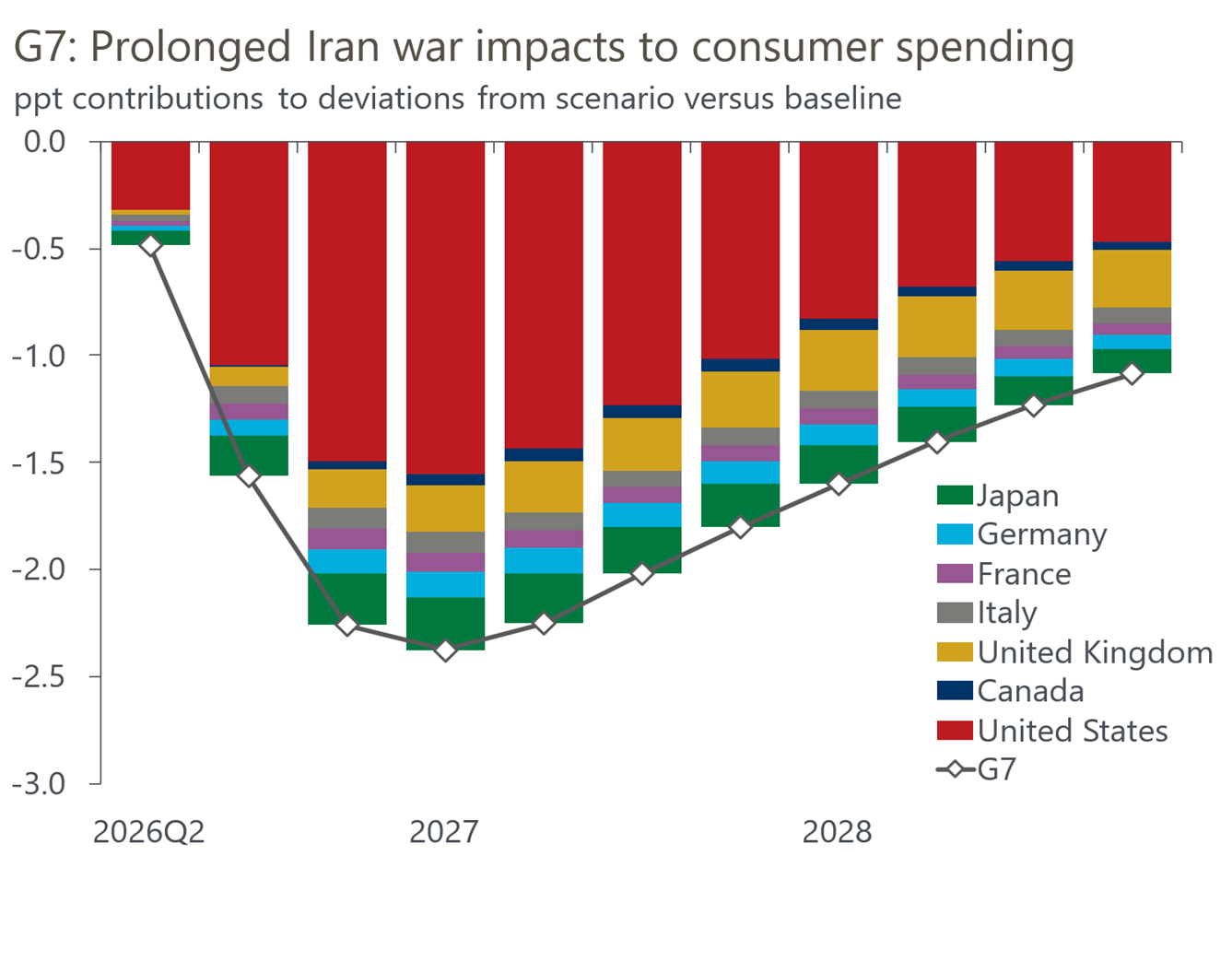

Oxford Economics has cut its 2026 G7 consumer spending forecast by 0.6 percentage points, warning that the drag from higher energy prices and financial spillovers will persist, leaving spending 0.3% below trend even after two years.

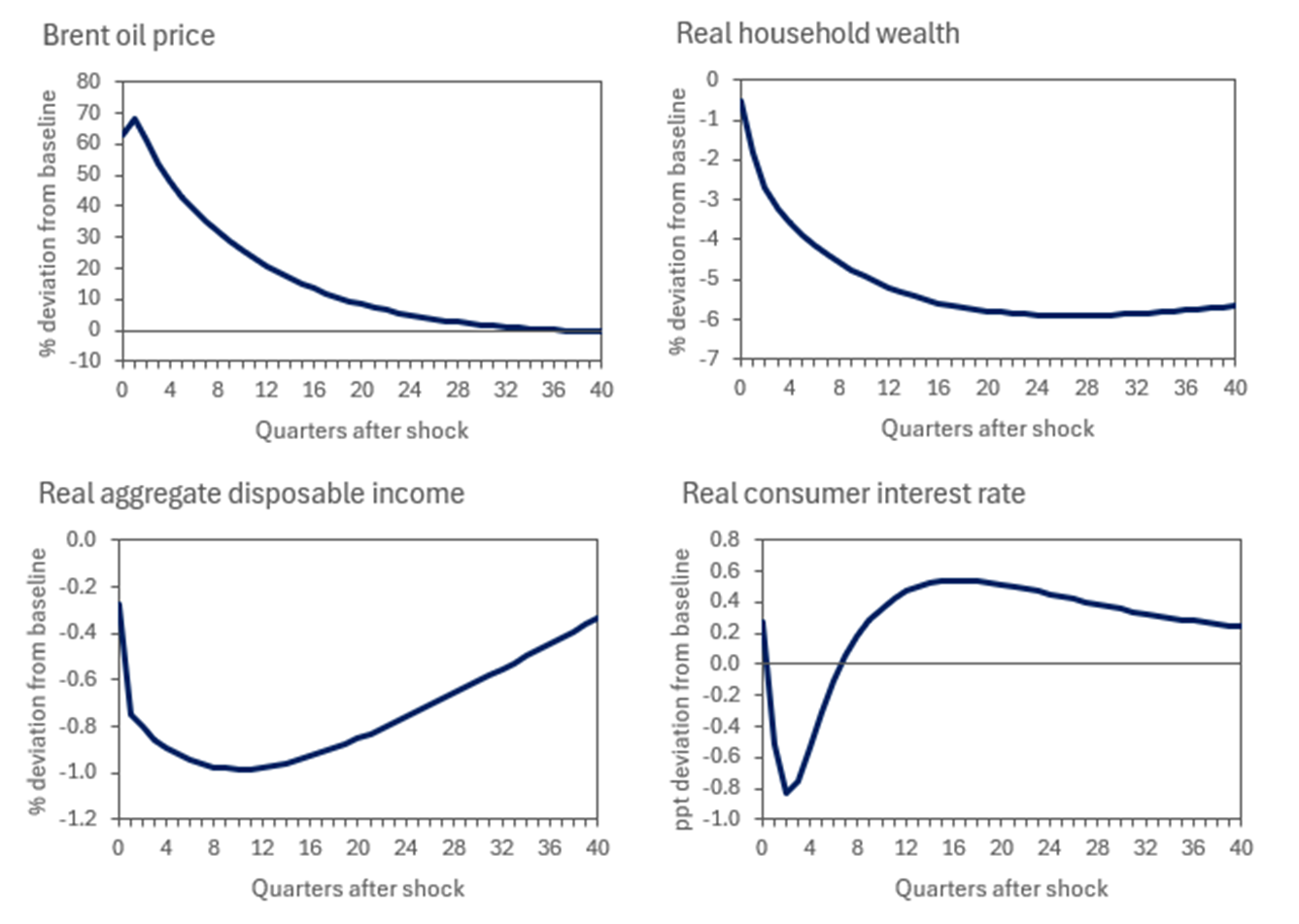

Brent crude is forecast to average $113 per barrel in the second quarter, up from $60 a month earlier, and remain elevated through 2026. “That shift marks a step change in household cost pressures rather than a temporary spike,” says Sweet.

“This is less than the percentage increase seen in 2022, but still unusually large outside periods of war or major geopolitical disruption,” Sweet said.

Not just oil: a broader inflation shock

The hit to consumers extends well beyond fuel costs. Higher energy prices are feeding through into broader inflation, eroding real disposable income and tightening financial conditions simultaneously.

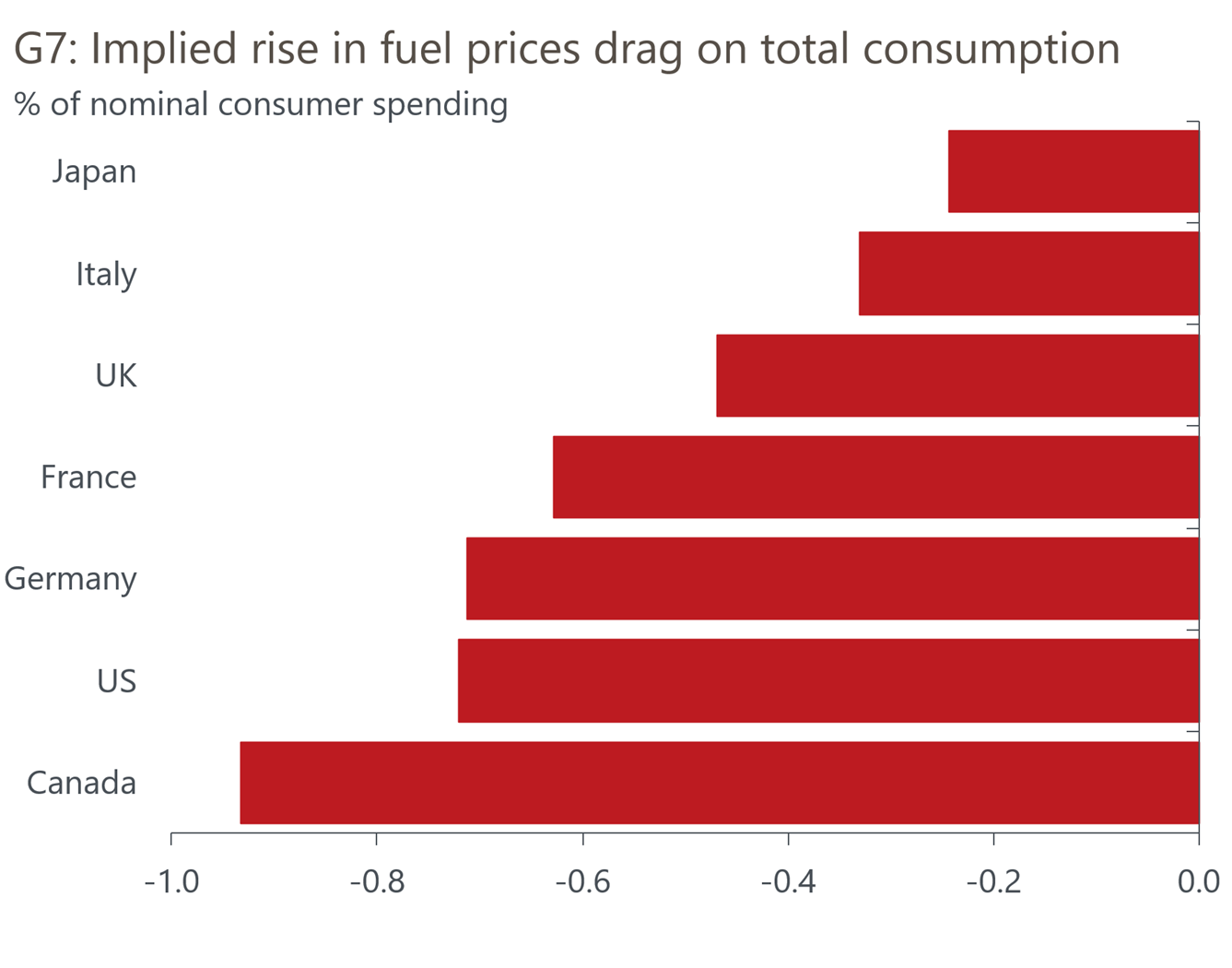

A useful proxy illustrates the scale of the squeeze. In the US, every $0.01 increase in petrol prices reduces consumer spending by $1.5bn over a year if sustained, according to Oxford Economics.

But Sweet cautioned that such rules of thumb understate the true impact. “Non-linearities mean that the larger the rise in oil prices, the larger the hit to consumer spending,” he said, adding that behavioural lags further complicate the adjustment.

This is not just an oil shock — it is a full-spectrum cost of living squeeze. Everything is being affected as the shock slowly spreads down supply chains as the crisis virus takes hold.

The most quoted example is food: the reduction in gas supplies feeds through the fertiliser production in a few months as stockpiles dwindle making it unavailable to farms in at the start of planting season now, which will reduce yields this autumn, leading to a food price shock at the end of this year and fuel a growing inflation shock that will force central banks to hike rates spilling into slower growth next year.

Financial markets amplify the hit

The direct income shock is only part of the story. Declining equity markets and bond markets that have been turned on their head, as expectations of rate cuts suddenly turn into expectations of rate hikes. These blows are amplifying the drag on consumption, especially in the US where the wealth-factor from a long bull-run on stock markets plays an important role. Discretionary categories of consumer goods are likely to take the biggest hit as a result.

Global equity markets have already fallen around 10% from recent peaks, weakening household balance sheets. “The knock-on effects of an oil-price shock… disproportionately affect discretionary big-ticket items,” Sweet said.

Higher real interest rates are reinforcing this dynamic by making saving more attractive relative to spending, while falling consumer confidence is driving precautionary behaviour. Conversely, the real estate sector will be adversely hit as home-buying is getting more expensive than ever.

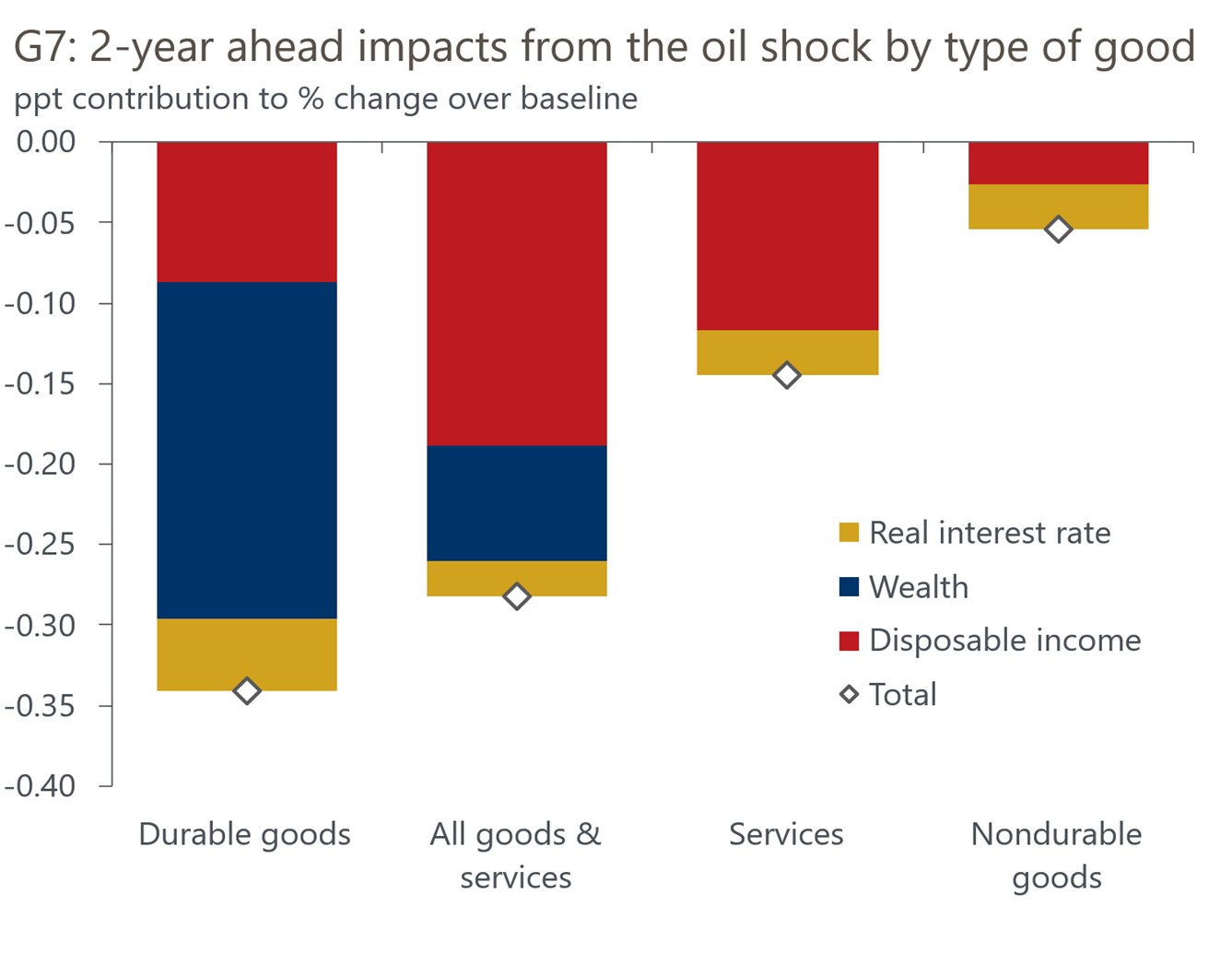

“The wealth channel accounts for the majority of the persistent drag on durables, well beyond the initial income shock,” Sweet added.

Durable goods take the deepest hit

Durable goods are expected to see the sharpest and most persistent decline. Spending on items such as cars is projected to remain 0.35% below trend even after two years.

“These goods typically require financing and are usually the first purchases consumers delay when uncertainty rises or sentiment sours,” Sweet said.

Higher fuel prices are also influencing purchasing decisions, with consumers delaying purchases or reassessing vehicle types. The US and Canada are particularly exposed due to higher vehicle ownership rates, while France and Italy are less sensitive given lower per-capita car sales.

One of the really big winners is expected to be the sale of EVs. The sale of electronic vehicles already hit critical mass before the war in Iran broke out as quality soared and costs fell. But now EVs have become mainstream: sales of EVs overtook standard petrol cars in the EU for the first time in December 2025, according to the European Automobile Manufacturers’ Association. Soaring petrol costs will only accelerate that trend now. Asian electric vehicle makers are seeing a surge in demand as well.

US wealth effects in focus

The US stands out as the most vulnerable G7 economy due to its reliance on financial markets as a driver of consumption. “Our research shows stocks have become the dominant driver of US consumption over the past 15 years, eclipsing housing,” Sweet said. With equity markets already down around 10%, that transmission channel is now active and likely to amplify the slowdown.

Canada and the UK, by contrast, are more exposed to interest rate transmission due to high household debt and the prevalence of floating-rate mortgages.

Germany and Italy are less sensitive, reflecting lower debt levels and more widespread use of fixed-rate lending structures.

Essentials hold up, but cracks are forming

Spending on non-durable goods and essential services is proving more resilient, but not immune. Categories such as food, fuel and healthcare show a muted response to oil shocks, but food prices will probably be only affected later this year as the transmission channel from high gas prices to falling harvest yields is long and slow.

The discretionary segments within services are already under pressure. Air travel, leisure and dining are also among the first areas where consumers cut back. Aviation fuel prices have already spiked as while crude is trickling out of the Gulf, refined products are not. The impact of the Gulf war is unevenly spread across the different oil product categories.

As the inflation shock starts to take hold, households are responding to uncertainty by cutting non-essential expenditure. “There’s another shift in consumer spending… as budgets tighten, consumers trade restaurant meals for groceries,” Sweet said.

No economy is insulated

US President Donald Trump has boasted that the US is insulated from the energy price shock as the US is a net exporter of energy and is unlikely to suffer from the shortages that will affect Asia the most. Commenting on the closure of the Strait of Hormuz, Trump said: “We don’t use it.”

But even the US will not be shielded from the shockwaves spreading out around the world. US and Canadian consumers still face global fuel prices, which feed directly into petrol and diesel costs regardless of domestic production. As IntelliNews has reported in the past, as commodities are fungible, if the price of petrol rises in Europe due to shortages, that will push up the price in the US too, as oil producers have the option of exporting to Europe to capture the bigger profits, even if the US is in surplus. It’s another aspect of the crisis virus spreading the infection of the shock around the world.

“The US shale revolution increased supply… but it didn’t decouple US pump prices from global oil prices,” Sweet said.

Across the G7, the impact varies depending on energy dependence, tax structures and household balance sheets, with European economies facing additional complexity due to its diesel exposure.

Risks skew to the downside

Risks remain tilted toward a more severe outcome, particularly if the conflict leads to sustained supply disruption.

In a downside scenario where Brent crude exceeds $150 per barrel for four months alongside refined product shortages, G7 consumer spending could undershoot the baseline by up to 2.2 percentage points, according to Oxford Economics calculations.

“The asymmetry is stark,” Sweet said. “The severity will be determined not only by how much oil prices rise and for how long, but also by the secondary effects on wealth and real interest rates.”

Unlock premium news, Start your free trial today.