Helium shortage threatens semiconductor industry

Qatar’s gas disruption is tightening the supply of helium, a natural gas byproduct that is crucial for semiconductor manufacturing and medical imaging, rapidly pushing up prices.

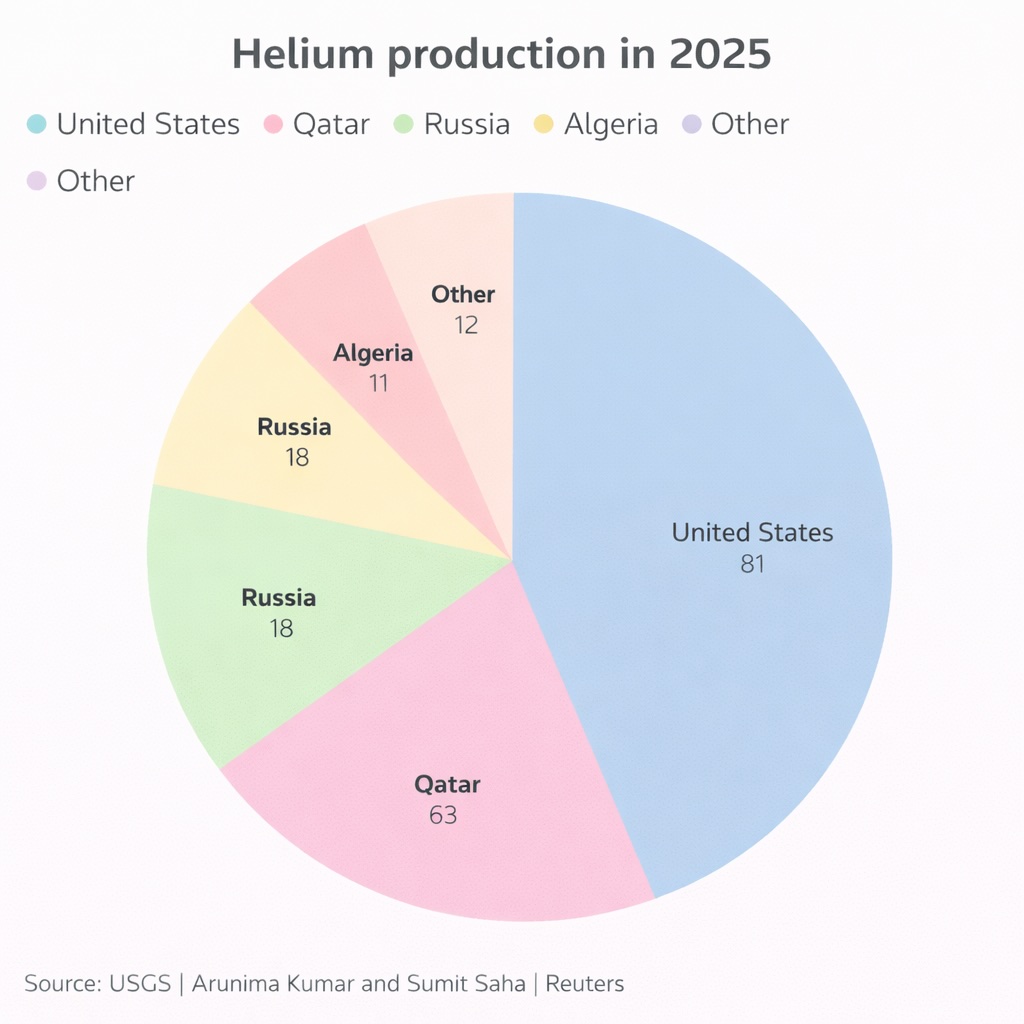

Qatar is the world's second-largest helium producer, supplying a third (33%) of global output, or 63mn cubic metres in 2025.

The country shut down its Ras Laffan facility, the world's largest LNG plant, at the start of Operation Epic Fury with force majeure declarations, breaking its supply contracts. That has taken 5.2mn cubic metres of helium off the market each month. The disruption has already doubled helium prices since the Iran war began on February 28.

There are alternative suppliers. The US is the world’s largest helium producer and has some buffer capacity. Algeria and Russia produce meaningful volumes. Poland is the only producer in the EU and has output that covers about 8% of the region’s demand. The EU sources roughly 40% of its helium from Qatar, Bloomberg reports. Air Liquide SA’s has an underground helium storage facility in the German city Gronau-Epe with a capacity of around 47mn cubic meters per year providing a temporary buffer for now.

Some overland rerouting from Qatar through Oman and Saudi Arabia is theoretically possible but the capacity is limited.

If disruptions last 60 to 90 days, experts say prices could surge another by 25-50%, potentially exceeding $2,000 per thousand cubic feet, or more than four-times pre-war levels.

Unlike oil, as the helium molecule is so small it is extremely hard to stockpile as the molecules can escape even the most sophisticated storage systems.

Moreover, as helium has the lowest freezing point of any element – only four degrees above absolute zero – it cannot be liquidified. The global supply chain operates on roughly 45 days of buffer before existing inventory boils off, so most is produced on demand as a by-product of natural gas extraction and liquefaction.

Semiconductor production in danger

In the same way that the halt of exports of fertilisers from the Gulf threatens food production this year, the halt of helium exports threatens the tech sector. If helium supplies dry up then the world’s semiconductor fabs will have to shut down production.

The gas is an essential part of the chip etching process. Semiconductor manufacturing requires ultra-pure helium for wafer cooling in lithography and for leak detection in sub-5-nanometre chip fabrication. Taiwan-based Taiwan Semiconductor Manufacturing Company (TSMC), Samsung, and Intel cannot produce advanced processors without it.

“Asia’s semiconductor supply chain faces rising tail risk from helium tightness as the Iran conflict drags on and Qatar’s natural gas disruption persists,” Fitch Ratings said in a note on March 17. “Credit risk would worsen if supply shortages exceeded inventory buffers, resulting in higher-cost sourcing, increased working-capital needs and production prioritisation.”

Taiwan’s major chipmaker TSMC is the most exposed to the shortage of helium. The company has said operations remain normal for now and that inventories and supply are manageable.

Taiwan’s Economic Affairs Ministry said 22 liquefied natural gas cargoes for March and April have been scheduled and domestic oil, coal and gas inventories are above statutory safety levels, implying no immediate gas supply issue. The Ministry framed the Iranian conflict as a “controllable risk” for Taiwan’s semiconductor sector.

“That supports near-term sentiment, but we believe medium-term risk exists if the disruption persists and replenishment cycles become harder to manage,” Fitch said.

Other less critical technologies also make use of helium. MRI machines require liquid helium to cool superconducting magnets to near absolute zero to perform their scans. Aerospace depends on helium for purging rocket fuel systems, pressurising tanks, and testing for leaks in systems where failure means explosion. Fibre optic cable manufacturing requires helium atmospheres. Quantum computing research also requires helium-3 isotopes for cryogenic cooling.

TSMC produces about 90% of the world’s most advanced logic chips and is the sole supplier for Nvidia Corporation’s AI accelerators and Apple Inc.’s iPhone processors. Any disruption would ripple through the tech sector in a semiconductor market expected to reach $1 trillion in sales this year and complicate around $650bn in planned artificial intelligence investments, Bloomberg reported on March 17.

“A disruption in the Strait of Hormuz wouldn’t automatically halt chip production, but it could ripple through power costs, materials supply, and the economics of building AI infrastructure,” Shawn Kim, Head of Asia Technology Research at Morgan Stanley told Bloomberg.

Companies building energy-intensive infrastructure such as data centres may face higher operating costs and weaker returns if the conflict persists.

If the disruption is sustained over an extended period, helium shortages could force chipmakers to prioritize production of higher-margin AI chips over less profitable components, Bloomberg Economics analyst Michael Deng said. TSMC shares have shed about 7% since the beginning of the war in the Middle East, while global stocks have lost about 6%. The sector is already suffering from a historic shortage of memory chips, which is already forcing consumer companies to hike chip prices around the globe.

Crisis duration key

The duration of the conflict will be key. If it drags on the situation will rapidly deteriorate, says Fitch.

“Even if Qatar’s facilities restart, the helium shortage may not end quickly. Qatar’s energy minister says normal deliveries could take weeks to months to resume after the conflict ends. The lag would likely extend a “catch-up” period for shipping schedules and contract allocations, keeping spot prices elevated and increasing the likelihood of tighter supply discipline by industrial gas distributors,” says Fitch.

Qatar accounted for a fifth of the world’s LNG supplies, but other producers, notably the US, can partly step in to fill the breach, giving the shortage a geographic dimension, with SE Asia expected to suffer the most.

South Korea is the most vulnerable as it sourced 64.7% of its helium imports from Qatar last year, reports Fitch. Taiwan faces similar risks as it is equally dependent on Qatar for the majority of its helium. By contrast, Japan’s helium supply is less exposed. It sources about 50% of its supply from the US and 28%–33% from Qatar, and holds inventories in both the US and Japan.

Cost and issue, but not crucial

Cost pressure is a second-order issue in Fitch’s base case but matters in a prolonged disruption. Spot helium prices could spike by 50%–200% in severe shortage scenarios, while contract prices are typically more stable but could still rise 20%–40% on renegotiation. However, as helium costs represent a small share of the overall cost of production, semiconductor fabs are relatively immune to sharp spikes in the cost of helium.

Even so, the impact on overall cost of goods sold should be modest for larger manufacturers because helium generally comprises around 0.5%–1% of production costs.

Company credit at risk

If the Iran war drags on, company credit ratings could suffer, says Fitch.

“Should constrained flows persist long enough to exhaust buffers – potentially beyond about six weeks – manufacturers could face tighter allocation, higher procurement costs and increased working-capital needs and earnings volatility,” says Fitch. “This could, in more severe cases, force production rescheduling or prioritisation towards higher-value output.”

Offsetting these problems, supply tightness will push chip prices up and support margins for the large Fitch-rated memory chip producers, limiting the rating impact and building resilience for a more prolonged disruption. The big chip producers typically have longer-term helium supply contracts, larger inventories and higher helium-recycling rates that reduce net consumption and spot-market exposure.

“Mitigants include long-term contracts with diversified suppliers including the US, Russia and Algeria, advanced helium recycling systems (leading fabs can recycle around 80%–90%), strategic stockpiling and multi-sourcing. Larger, leading-edge manufacturers with robust recycling and established contract structures are better positioned than smaller operators with greater spot-market reliance,” Fitch said.

Unlock premium news, Start your free trial today.