BofA goes short on 2-month dollar/lira forward contract for 3.3% monthly carry return

Bank of America (BofA) Global Research analysts Mikhail Liluashvili and Hande Kucuk on May 26 advised shorting the 2-month USD/Turkish lira (TRY) forward contract amid the ongoing political turbulence in Turkey.

“We recommend going short USDTRY in the 2m forward at 48.8 (spot reference: 45.9, carry: c. 3.3% per month) and plan to hold it until maturity, when we will assess whether to re-enter the trade,” the analysts said in a research note subheaded, “Risk repricing improves entry point.”

“Domestic political uncertainty has created a more attractive entry point”

“Rising domestic political uncertainty has led to a repricing of risk, creating a more attractive entry point, in our view,” the BofA analysts also said.

The risks of the trade are much higher oil prices, a stronger broader USD, persistent local dollarisation, an intensifying geopolitical backdrop and resident capital outflows abroad.

Authorities remain firmly committed to keeping TRY devaluation below carry return

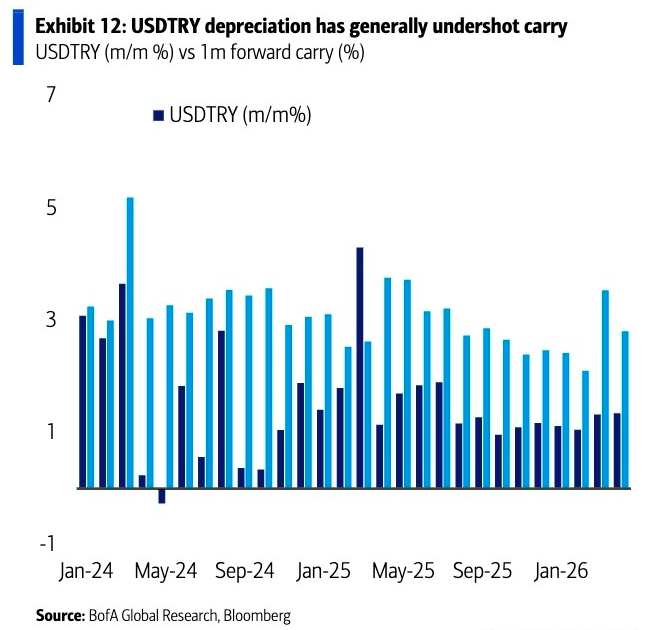

The authorities remain firmly committed to the real appreciation of the TRY against the USD while keeping the real policy rate in positive territory, according to BofA.

This means that the TRY should depreciate less than forwards imply. Indeed, the central bank has managed to consistently deliver depreciation that is lower than the monthly carry.

Chart: Monthly carry return versus lira devaluation.

Reserves exceed foreign positioning

Liquid FX reserves stood at $37bn as of May 15 and they could be further supported through the central bank’s use of gold-to-FX swaps. And, if needed, the authority could go to direct gold sales.

Usable reserves exceed the total forward foreign positioning, which stood at around $30bn as of May 15.

There is also some foreign positioning in the Turkish government’s domestic lira bonds, standing at $14bn. However, it tends to be difficult to fully liquidate such positions during periods of market stress and bond prices could fall if the global environment deteriorates further, according to BofA.

Equity positioning, which stands at about $44bn, also seemed to be sticky during such episodes, the analysts said.

Rising tourism revenues over the summer should support the current account for the duration of BofA’s trade. Economists at the bank do not expect a sustained current account surplus. However, seasonal improvements will be supportive to the BofA analysis.

“Authorities can contain local dollarisation”

Local dollarisation is a risk to the trade. However, the analyst duo believe the authorities can contain this, if need be, through policy rate hikes, macroprudential measures and continued real exchange rate appreciation.

Resident capital outflows are another risk. However, in BofA’s view, the current policy framework provides tools to mitigate these pressures.

Iran risk

If the conflict in Iran escalates, the authorities might need to increase the pace of depreciation. However, BofA would not expect this to happen immediately. And, the new pace should remain below the current carry in USD/TRY forwards for the next two months even in this scenario, in BofA’s view.

JPMorgan takes 55% USD-basis profit

Separately, JPMorgan said on May 29 that it has taken full profit on its core overweight position in the Turkish lira and shifted to a more tactical, short-term view.

Strategists, including Anezka Christovova, wrote in a note that the lira overweight had been a core position in its government bond index-emerging markets model portfolio since early September 2023, with only a brief interruption around Turkey’s March 2024 local elections.

The currency has delivered a 55% total return since September 2023.

JPMorgan had already reduced the overall size of its position on April 30.

Shift to a tactical stance

While noting that recent domestic developments present limited immediate risks to the currency and that Turkish authorities are highly likely to remain focused on keeping FX volatility low as a key policy tool, the strategists believe the risk-reward dynamic has changed.

Increased risk of snap election

A lower expected return profile moving forward, rising balance of payments funding requirements, potential pressure stemming from elevated global energy prices and an increased risk of early elections are the main drivers in JPMorgan’s shift to a short-term strategy.

In agreement with BofA

Any potential election-related dollarisation or near-term pressure is now better addressed through shorter-maturity lira carry positions rather than holding the long-term core overweight stance, JPMorgan also said.

Locals doubled JP

“Those who held Turkish lira money market funds between September 2023 and May 2026 achieved a 220% return. When converted to USD, that translates to a 95% return,” @e507 wrote in response to JP.

Credit card indebted Turks paying up to 4.55% per month

Currently, a Turk, indebted on credit cards, pays a monthly interest rate of between 3.11% and 4.55%. The range moved up to as high as 3.11-5.30% between March 2024 and July 2025.

Unlock premium news, Start your free trial today.