Turkish central bank revives FX swaps with local lenders as war pressures hit reserves

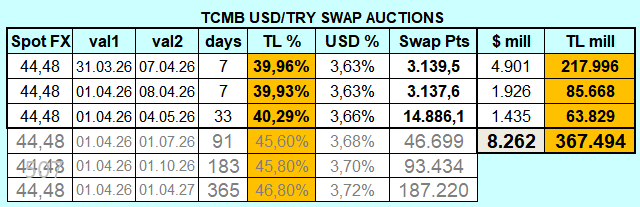

Turkey’s central bank on March 31 launched three FX swap auctions worth $10bn with local lenders, according to media reports.

A $5bn one-week auction was announced as value-today (same day or T+0 settlement), while a $2.5bn one-week auction was value-tomorrow and a $2.5bn one-month auction was also value-tomorrow.

At the auctions, the central bank accepted $8.62bn of bids. In exchange, it absorbed Turkish lira (TRY) 367bn in liquidity from local lenders at a USD/TRY exchange rate of 44.48.

The value-today swaps worth $4.9bn are reflected in the official data set.

Table by @e507: Results of the central bank’s swap auctions held on March 31 and implied rates for longer maturities.

Identical rates, longer maturities

The implied lira interest rate in the auctions came in at 40%, in line with the current level of the central bank funding rate and market rates (TLREF).

Local banks will, meanwhile, benefit from longer term maturities compared to daily funding from the central bank and the interbank money market.

Another option for local lenders to access lira funding in exchange for dollars (when FX demand rises, they buy dollars to fix their currency risks) is the London offshore market.

However, foreign players have been closing their lira positions since the latest chapter in the US and Israel war with Iran was opened with missile strikes on February 28.

Lira scarcity

Since that day, Turkey’s central bank has sold more than $30bn to avoid a lira collapse amid similar portfolio outflows. In exchange, it absorbed lira held by local lenders.

| Portfolio outflows from Turkey | |||||||||||||

| Carry Trade Flows to Turkey (estimate) | Lira papers | Total | Residents' FX deposits | ||||||||||

| million USD | Turkish Banks Off-Balance Sheet FX Position | Turkish Central Bank's Total Swap Stock with Local Banks | Lira-settled FX Frowards | Turkish Central Bank's Net FX Derivatives Stock with Local Banks | Turkish Banks' Swap Stock with Foreign Counterparts (estimate) | Carry Trade Flows (estimate) | Cumulative Flow Carry | Domestic Government Bonds Weekly Flow | Equity Weekly Flow | Carry Plus Lira Papers | Cumulative Total | Currency-Adjusted Change | Cumulative |

| Feb 27 | 55,649 | -3,417 | 0 | -3,417 | 59,066 | ||||||||

| Mar 6 | 51,183 | -2,646 | 507 | -2,139 | 53,322 | -5,744 | -1,726 | -756 | -8,225 | 233 | |||

| Mar 13 | 45,517 | -1,695 | 804 | -891 | 46,408 | -6,914 | -12,658 | -2,878 | -322 | -10,114 | -18,339 | -1,215 | -982 |

| Mar 19 | 41,838 | -2,581 | 1,363 | -1,218 | 43,056 | -3,352 | -16,010 | -130 | -138 | -3,620 | -21,958 | 839 | -143 |

| Mar 27 | -2,416 | 4,195 | |||||||||||

| Mar 30 | -1,710 | 5,140 | |||||||||||

Table: Between February 27 and March 20 (covering the first three weeks of the Iran war), Turkey faced $22bn worth of portfolio outflows, while Turks’ FX deposits showed little change.

| Turkish central bank's net FX position | |||||||||

| A.1_FOREIGN ASSETS (Thousand TRY) | P.1_TOTAL FOREIGN LIABILITIES (Thousand TRY) | Net (A.1-P.1) | USD/TRY Buying | Net USDmn | 2. Aggregate short and long positions in forwards and futures in foreign currencies | 3. Other (specify) | Net (minus) swaps | Change (USD bn) | |

| Feb 27 | 9,324,614,981 | 5,683,765,634 | 3,640,849,347 | 43.59 | 83,525 | -16,408 | 3,467 | 70,584 | |

| Mar 19 | 7,934,307,764 | 5,780,880,425 | 2,153,427,339 | 44.13 | 48,797 | -16,354 | 1,952 | 34,395 | -36,189 |

| Mar 27 | 6,986,856,579 | 5,783,013,326 | 1,203,843,253 | 44.28 | 27,187 | ||||

| Mar 30 | 6,746,084,438 | 5,673,976,220 | 1,072,108,218 | 44.29 | 24,207 | ||||

| Gold price effect | ||||||||||||||

| A.1 Gold (Thousand TRY, gross) | Gross gold (Thousand USD) | A.11 Gross gold (gram) | Gold price (gram, TRY) | P.3213 Local banks' gold deposits (gram) | P.3112 Treasury 's gold (gram) | P.3232 Local bank's reserve requirement(gram) | P.4.2. Foreign banks' gold deposits (gram) | Swaps with local banks (USD mn) | Swaps with local banks (gram) | Net gold (gram) | Net gold (USDmn) | Net gold (USDmn with Feb 27 gold price) | Gold price effect | |

| Feb 27 | 5,993,390,409 | 137,494,618 | 822,521,242 | 7,287 | 32,569,588 | 26,936,640 | 185,453,800 | 29,999,999 | 3,417 | 20,441,201 | 568,002,416 | 94,949 | 94,949 | |

| Mar 19 | 5,126,709,172 | 116,172,879 | 771,576,811 | 6,644 | 30,400,488 | 23,769,555 | 188,601,185 | 29,999,999 | 2,581 | 17,142,037 | 515,947,621 | 77,684 | 86,247 | 8,563 |

| Mar 27 | 2,416 | |||||||||||||

| Mar 30 | 1,710 | |||||||||||||

Table: The net FX position of the Turkish central bank fell by $36bn in the first three weeks of the war. However, $9bn was ascribed to the gold price fall, suggesting net reserve sales of $28bn.

As a result of dollar sales, the central bank has once again created a dearth of lira in the banking system. The ‘lira’ in question here is central bank money, which is different from the currency used by non-bank economic actors. Details of the difference referred to are here.

Hard to believe, but no crisis yet

For the sake of managing its reserve liquidity, the central bank has also sold some of its gold reserves in addition to employing gold-to-dollar swaps on the London market.

The nosedive in gold prices has also created sharp declines in the central bank’s reserves.

The visible declines coupled with gold sales/swaps in addition to the revival of swaps with local banks and sales of lira-settled forward contracts to local banks may sound like a crisis.

However, the actual situation is still far from a crisis. It remains within the borders of reserves and liquidity management.

A reminder of the bad old days

In 2018, following the currency crisis, Turkey’s central bank launched derivative transactions to finance its interventions in the currency market.

At its November 2023 peak, the central bank’s open swap stock with local banks reached $64bn.

In June 2023, the current ‘orthodox’ economic management team took the wheel. Following the local elections held in March 2024, the central bank aggressively cut the volume of its derivatives stock, while building up its reserves thanks to portfolio inflows along with declines in FX deposits and increases in FX loans at local banks.

As a result, the swap stock with local banks declined from $58bn at end-March 2024 to zero as of July 31, 2024.

Moreover, the central bank on August 2, 2024 introduced reverse swap auctions (at spot, banks deposit lira at the central bank in exchange for FX and gold) as a new sterilisation tool.

As of March 30, the central bank’s open reverse swap stock with local lenders (made up of only gold swaps) stood at $1.71bn.

Unlock premium news, Start your free trial today.