Fitch stress test sees no Turkish bank failure even if Iran conflict drives lira to USD/75

Turkish banks’ would overcome severe effects of a prolonged Iran conflict without needing to ask for additional capital injections from their shareholders, according to the results of a stress test conducted by Fitch Ratings.

Under the most severe scenario, in which the USD/Turkish lira (TRY) pair hit the 75-level and the non performing loan (NPL) ratio climbs to 7.5% by end-2026, only one bank, namely state lender Halkbank (HALKB), would breach legal reserve requirement criteria, the rating agency also said in a press release.

Good and bad headlines

Perhaps to catch interest, the press release was headed “Turkish Banks’ Capital Buffers Could Be Tested on Significant Stress”.

Fitch conducted the stress test for a report that it prepared in response to questions from investors over its analysis of the likely impacts of a prolonged Iran war.

In March, IntelliNews published an article headlined, “What no crisis!? Turkey is so far riding out economic shocks of the Iran war”.

“Newsrooms with an eye on Turkey have been lately struggling to believe that since the end-of-February onset of ‘Gulf War III’, there’s so far been hardly a trickle of articles suggesting big crises are taking hold in its economy,” this publication noted.

“No crisis” headlines do not attract clicks. Thus, “Capital Buffers Could Be Tested on Significant Stress” headlines are preferred.

In a separate section of its report on questions from investors, Fitch observed that recent strength seen in the dollar could unwind if oil prices fall back.

Fitch’s test for “stress”

Based on Basel III criteria, Turkish banks are obliged to comply with the legal minimum common equity Tier 1 (CET1) ratio, which stands at 4.5%.

Fitch Ratings said it “stress-tested” the capital adequacy of nine major Turkish banks using USD/TRY rates and NPL ratio increases significantly above base-case expectations for end-2026.

In its base case, Fitch sees the USD/TRY rate at 49.5 and the Turkish banking industry’s NPL ratio at 3.4%. The rating agency views these two indicators as the key risks to the local banking industry’s solvency.

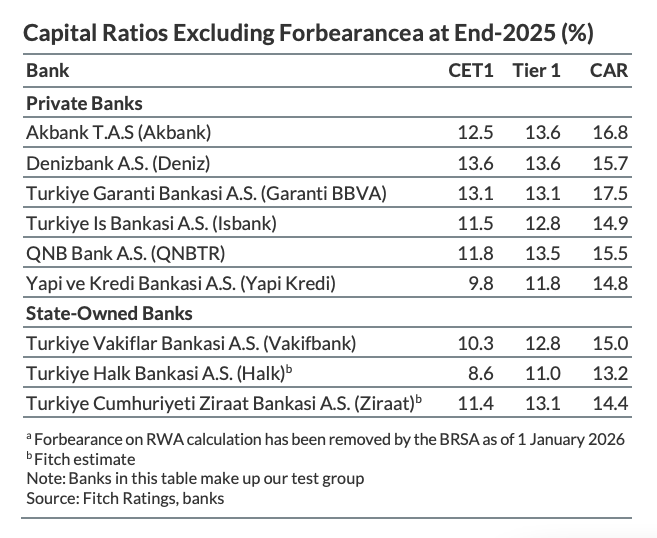

Table: Ratios as of end-2025.

Removal of forbearance on the calculation of FC risk-weighted assets (RWAs) is key to the realisation of the impact of depreciation as the exchange rate used for calculations would change, Fitch noted.

Most Turkish banks have, meanwhile, also been monitoring and reporting capital ratios net of forbearance.

Range of scenarios

Credit risks from the Iran conflict are contained under Fitch’s base case for a short disruption.

The rating agency concluded that a more prolonged conflict could trigger a sharp lira depreciation via political interference in the current policy set should there be significant pressure on the sovereign or economic spillovers from regional instability.

Under the mildest scenario of a USD/TRY rate of 60 and a 2.5pp rise in NPL ratios, no bank breaches legal minimum capital requirements.

Under the most severe scenario mentioned above, only one bank breaches the legal minimum CET1 ratio, breaching it by 108 basis points.

The buffer currently averages 5.5% of average gross loans for state-owned banks and 7.2% for private banks.

Fitch estimates that a 10% lira depreciation would reduce the aggregate CET1 ratio of all nine banks by around 50bp while a 1pp increase in the NPL ratio would reduce it by around 46bp by end-2026.

Sector NPLs accounted for 2.5% and 2.7% of gross loans at end-2025 and mid-April 2026, respectively.

Fitch sees a rise in NPLs throughout 2026, although at manageable levels, driven by unsecured retail and SME portfolios (given their sensitivity to economic cycles and high lira interest rates).

No policy response, shareholder support assumed

In the given scenarios, the rating agency has assumed that bank managements will not take any measures against escalating risks by end-2026. Additionally, its assumption is that Turkey’s government will not introduce any additional regulatory forbearance measures and shareholders of the banks will not provide any support.

Fitch factors ordinary support from shareholders of foreign-owned banks (namely QNB Turkey (QNBTR), Denizbank and Garanti BBVA (GARAN)) and from the Turkish authorities for state-owned banks into its ratings.

“These could mitigate capital erosion before potential breaches but are not reflected in the stress test results,” the rating agency noted.

As of January 1, Turkey’s banking watchdog BDDK had removed two key forbearance measures on the calculation of the banks’ risk-weighted assets (RWAs). Fitch estimated the capital ratios would now decline by 170–200bp on average.

“Forbearance may be reintroduced under significant stress or exchange-rate volatility to support capital ratios,” the rating firm said.

Profits provide buffers

Turkish banks can absorb credit losses through their income statements on pre-impairment operating profit, Fitch also said.

Pre-impairment operating profit buffers are often stronger at private banks, standing at 7.2% of average gross loans at end-2025, than at state-owned banks, standing at 5.5%. They are strongest at QNB Turkey at 9.1% and weakest at Halkbank at 3.5%.

Unlock premium news, Start your free trial today.