Central Europe's new convergence challenge

Poland aims to catch up with the United Kingdom in GDP per capita adjusted for price levels within five to six years, Finance and Economy Minister Andrzej Domański said this week, setting out one of the most ambitious convergence targets yet voiced by a Central European government.

Speaking at the Warsaw Stock Exchange shortly after Prime Minister Donald Tusk declared that Poland was closing the gap with advanced economies such as Japan, New Zealand, Israel and Spain, Domański said Warsaw should now aim higher.

“I am taking on the challenge of catching up with the United Kingdom within 5-6 years in GDP per capita adjusted for price levels,” Domański said on February 18, framing the goal as the next stage of Poland’s post-communist transformation.

The pledge reflects how far the country has come since joining the European Union in 2004. Poland’s nominal GDP surpassed $1 trillion in 2023 for the first time, according to World Bank data, and is projected to rise further in 2025. Since EU accession, its economy has expanded more than fivefold in dollar terms, far outpacing the EU average.

Investment to replace consumption

Poland’s economy grew by 3.6% in 2025, accelerating from 3% a year earlier, preliminary data from the statistics office GUS showed. Growth was driven by strong domestic demand: private consumption rose 3.7% and investment increased 4.2%, rebounding from a contraction in 2024.

But Domański made clear that the old formula - consumption-led growth supported by rising wages and low unemployment - is no longer enough.

“In the past, GDP growth in Poland relied mainly on consumption,” he said. “This year we also expect consumption to remain an important driver of growth … but it is investment that will be the engine powering the Polish economy in 2026.”

He forecast investment growth of around 10-11% this year, more than double the pace of 2025. Planned outlays include PLN200bn for defence, PLN25.2bn for roads, PLN14bn for rail, PLN15bn for energy-efficiency upgrades and PLN8bn to kick-start construction of Poland’s first nuclear power plant. Further funds are earmarked for a new central airport, maritime infrastructure and local government projects.

This reflects both domestic pressures and a broader regional shift. For much of the post-pandemic period, Central and Eastern Europe (CEE) expanded on the back of rapid real wage growth that fuelled household spending. But with wage growth moderating and labour shortages pushing up costs, investment — particularly in automation, defence and energy — is set to play a bigger role.

Poland has recently outpaced its Central European peers, according to a recent note from Capital Economics, which Emerging Europe economist Nicholas Farr attributed partly to a “rebound in investment … supported by the unlocking of EU funds”.

Preliminary figures indicate its GDP growth picked up to 3.6% in 2025. Looking ahead, PKO BP said in a note that while “Household incomes are set to continue rising rapidly, supporting consumption … the main engine of growth will be investment, which we forecast will increase by about 12% in 2026.”

Behind Western Europe

Despite the catchup and typically faster growth, the new EU member states in Central and Southeast Europe remain behind almost all of their West European peers in terms of GDP per capita.

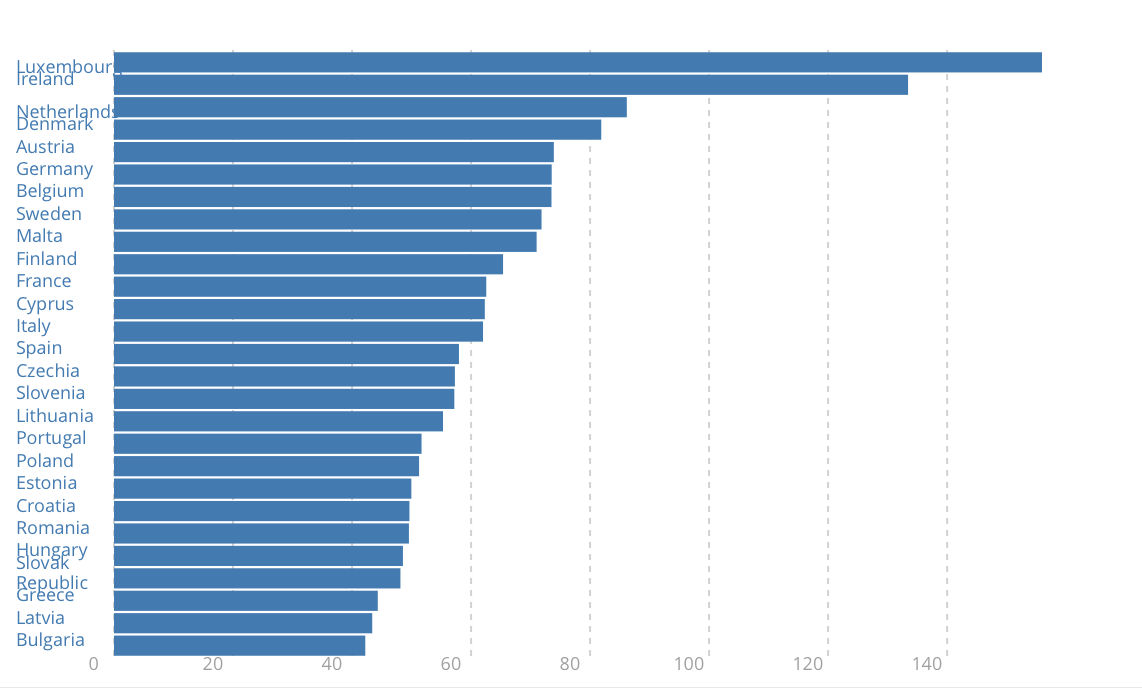

World Bank data shows that only Czechia, Slovenia and Lithuania have overtaken West European EU member Portugal in GDP per capital in purchasing power party (PPP) terms, more than 20 years after they joined the EU. Most of the Central and Southeast European countries now beat Greece on that metric.

GDP per capita, PPP (current international $). Source: World Bank.

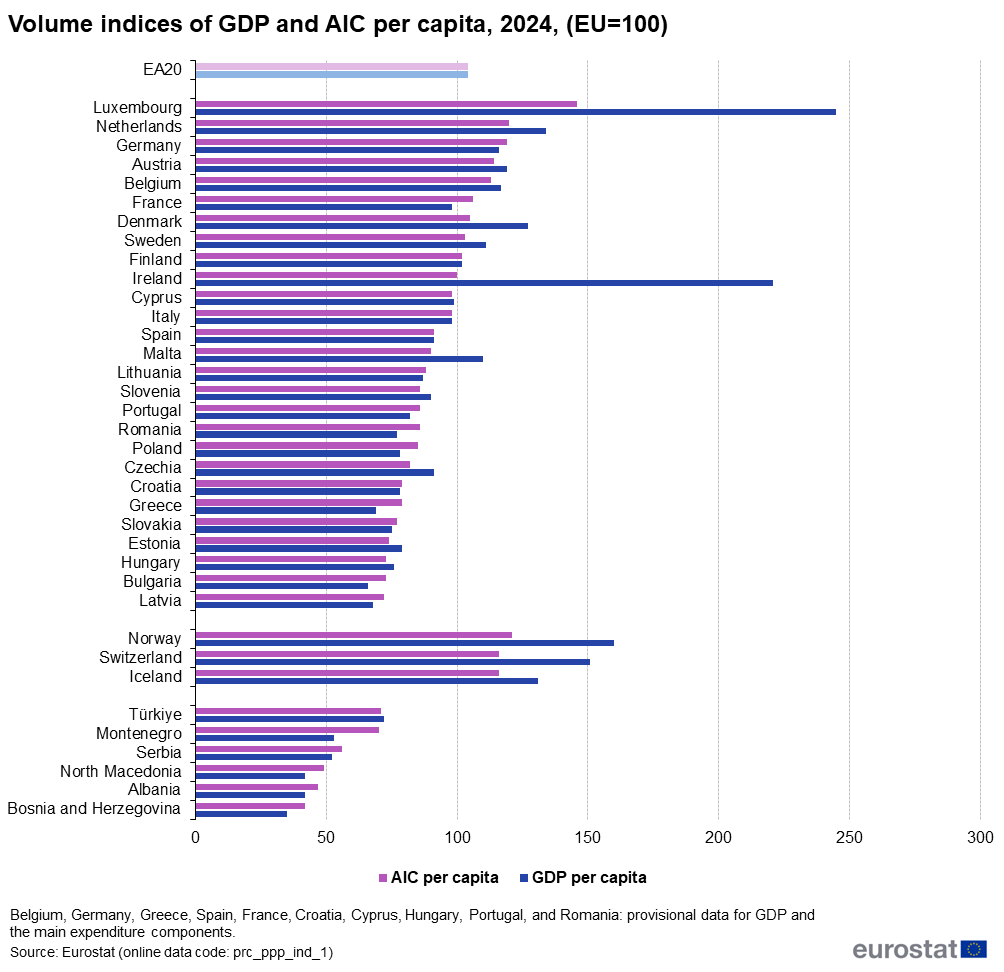

Eurostat GDP per capita data shows a similar picture, as does Actual Individual Consumption (AIC) per capita data, used to compare the relative welfare of consumers across countries, from the EU’s statistics office.

Source: Eurostat.

The Czech economy has long been considered one of the region’s most prosperous, underpinned by deep integration into German supply chains, a strong industrial base and the EU’s lowest unemployment rate. Over three decades, Czech living standards have nearly tripled, and the country has overtaken Portugal and Greece in GDP per capita terms.

Slovenia also remains one of the most prosperous post-socialist states, partly a legacy of its past during Yugoslav era. It was the first Southeast European country to join the EU, the first emerging European country to join the eurozone and the first from the region to switch from borrower to donor status at the World Bank. It overtook Portugal in GDP per capita terms at the start of the 2005-08 boom, then Greece in 2012.

In the Baltics, Lithuania has emerged as a fast converger. It now boasts the highest GDP per capita in purchasing power terms among the three Baltic states and has steadily narrowed the gap with the EU average since the global financial crisis, supported by foreign direct investment and growth in high-value services.

At the other end of the spectrum, Bulgaria and Romania, while still the poorest EU members in per capita terms, have also posted strong catch-up growth over the past decade, steadily raising their share of the EU average even if the absolute gap remains wide.

New model required

Poland’s ambition to reach UK levels within a decade would mark a qualitative leap in convergence, especially as the UK itself remains one of Europe’s largest and wealthiest economies.

Economists have warned that sustaining rapid catch-up will require a new growth model for the Central and Southeast European region.

The Vienna Institute for International Economic Studies (wiiw) said that the export-led model that defined the region’s success — low-cost manufacturing integrated into Western European supply chains — is becoming obsolete. Rising unit labour costs have eroded competitiveness, while geopolitical fragmentation is reshaping trade patterns.

“We are in the age of geoeconomics,” wiiw deputy director Richard Grieveson said at a recent briefing. “The old growth model is over, and a new one is emerging.”

According to wiiw’s winter forecast, the 10 EU countries of Central and Eastern Europe are expected to grow by around 2.6-2.7% in 2026-27, almost twice the projected euro zone pace. Poland is seen as the fastest-growing large economy in the bloc, with growth of 3.7% in 2026.

However, the composition of that growth is shifting. Private consumption is losing momentum, while private and public investment are set to take the lead. Defence spending, the green transition and automation are likely to push investment to a higher share of GDP across the region.

At the same time, exports are becoming a smaller share of output in many countries, as weaker German demand and geopolitical tensions weigh on trade.

For Poland, the challenge will be to ensure that its planned investment surge translates into productivity gains rather than simply higher imports. Large infrastructure and defence outlays can boost growth in the short term, but long-term convergence depends on innovation, skills and domestic value added.

As Warsaw sets its sights on British living standards, both Poland and the broader region face a similar question: whether it can move beyond being Europe’s “extended workbench” and build a more technology-driven, higher-productivity model.

Unlock premium news, Start your free trial today.